Accounting Treatment of Goodwill in case of Dissolution of Firm (original) (raw)

Last Updated : 8 Jun, 2026

Goodwill is the monetary value of the reputation, customer loyalty, business connections, and other advantages that enable a business to earn higher profits than a normal business. It is an intangible asset of the firm. In a partnership firm, goodwill belongs to the firm as a whole, and each partner has a claim on it according to their profit-sharing ratio. During the dissolution of a partnership firm, goodwill is treated like any other asset. It is realized (sold or valued), and the amount realized is distributed among the partners according to their profit-sharing ratio, after settling liabilities and other dissolution-related adjustments. So, the key idea is that goodwill represents the value of the firm's established reputation and is shared by all partners in proportion to their rights in the business.

**Accounting Treatment:

**A. When Goodwill appears in the Balance Sheet of the Firm:

**1. On transfer to Realisation Account:

**Journal Entry:

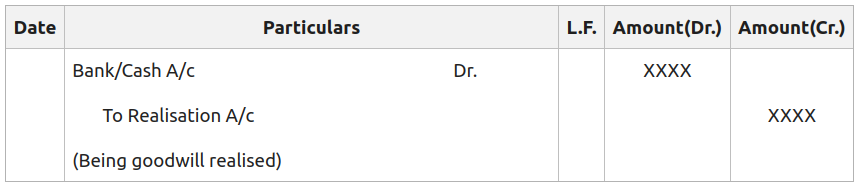

**2. Realisation of Goodwill:

****(i) Goodwill realised in cash:**

**Journal Entry:

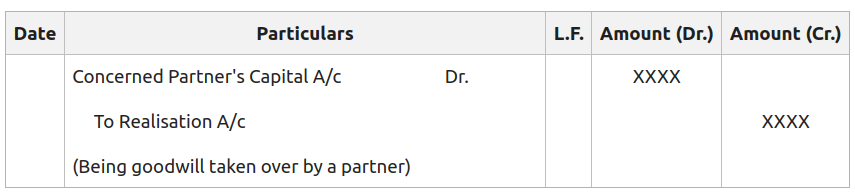

****(ii) If any of the partners take over the Goodwill and agrees to pay for Goodwill:**

**Journal Entry:

B. When Goodwill does not appear in the Balance Sheet of the Firm:

**1. On transfer to Realisation Account:

**No Entry

Note:

Goodwill doesn't exist in the books of the firm, so nothing is to be transferred to Realisation Account.

**2. Realisation of Goodwill:

****(i) Goodwill realised in cash:**

**Journal Entry:

****(ii) If any of the partners take over the Goodwill and agrees to pay for Goodwill:**

**Journal Entry:

Illustration:

Kapil, Rohit, and David are partners sharing profit and losses in a ratio of 2 : 1 : 1. On 31st March 2020, they decided to dissolve the firm. Their balance Sheet as on the same date stood as :

Additional Information:

1. Half of the Goodwill realised for ₹ 20,000 and half is taken over by Rohit for ₹ 20,000.

2. Assets Realised for:

Land and Building: ₹ 2,00,000

Plant: ₹ 1,00,000

Machinery: ₹ 56,000

Debtors: 50% of Book Value

3. Realisation Expense cost ₹ 4,000.

Prepare Realisation Account, Partner's Loan Account, Partner's Capital Account and Cash Account and Pass necessary Journal Entries.

**Solution:

**Working Note:

1. Value of Asset Realised:

Goodwill (Half) = 20,000

Land and Building = 2,00,000

Plant = 1,00,000

Machinery = 56,000

Debtors = 96,000\times\frac{50}{100}~=~48,000

**Total = 4,24,000