Difference between Profit and Loss Account And Profit and Loss Appropriation Account (original) (raw)

Last Updated : 28 Apr, 2026

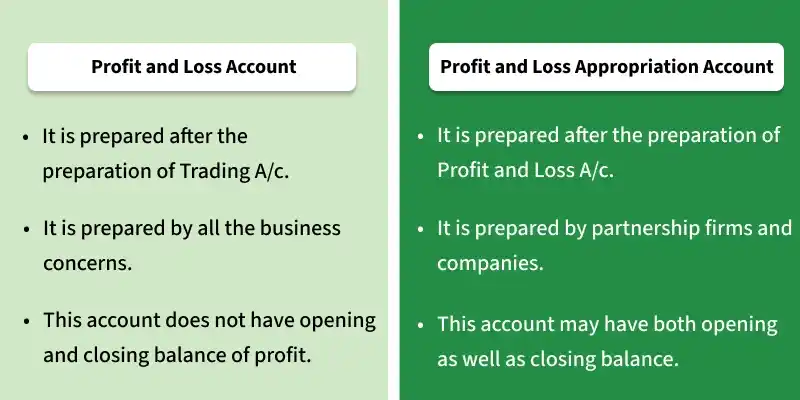

After preparing the Trading Account, businesses prepare the Profit and Loss Account to determine the final profit or loss. After this, especially in partnerships and companies, the Profit and Loss Appropriation Account is prepared to show how the profit is distributed among owners or shareholders

Profit and Loss Account

A financial statement that shows the net profit or net loss of a business during a specific accounting period. It is prepared to ascertain profit or loss, record all indirect expenses and incomes, and evaluate the overall performance of the business. The debit side includes expenses such as salaries, rent, depreciation, insurance, and office expenses, while the credit side includes incomes like gross profit, commission received, interest received, and discount received. If the credit side exceeds the debit side, the result is a net profit; otherwise, it results in a net loss

Profit and Loss Appropriation Account

shows how the net profit of a business is distributed among partners or shareholders. It is prepared to allocate profit, provide for reserves and dividends, and show retained earnings. The debit side includes appropriations such as interest on capital, partner’s salary, transfer to reserves, and dividends, while the credit side includes net profit from the Profit and Loss Account and interest on drawings. This account is important because it ensures fair distribution of profit, helps maintain reserves, fulfils partnership agreement terms, and provides returns to shareholders.

Difference between Profit and Loss Account And Profit and Loss Appropriation Account

| **Basis | **Profit and Loss Account | **Profit and Loss Appropriation Account |

|---|---|---|

| **Meaning | Shows net profit or loss | Shows distribution of profit |

| **Purpose | To calculate profit | To appropriate profit |

| **Preparation | Prepared first | Prepared after P&L Account |

| **Items | Includes expenses and incomes | Includes profit distribution items |

| **Applicability | Applicable to all businesses | Applicable to partnerships and companies |

| **Focus | Earning of profit | Distribution of profit |

| **Type of Items | Revenue items (expenses & incomes) | Appropriation items (not expenses) |

| **Effect on Profit | Determines net profit or loss | Does not affect net profit, only distributes it |

| **Mandatory | Compulsory for all businesses | Not compulsory for all (mainly partnerships & companies) |