Guarantee of Minimum Profit to a Partner: Journal Entries & Example (original) (raw)

Last Updated : 28 Apr, 2026

It means that a partner is assured a fixed minimum amount of profit, called the guaranteed amount. If the partner’s actual share of profit is less than this amount, the deficiency is made good by the partner or partners who have given the guarantee. The partner receiving the assurance is known as the guaranteed partner, while those who cover the deficiency are called guaranteeing partners. The deficiency is shared among them either in their profit-sharing ratio or in an agreed ratio . Guarantee of Minimum Profit to a Partner can be understood in the following cases:

- **When no information about the Guaranteeing Partner and the ratio in which the deficiency amount has to be borne is given: In this case, any deficiency in the Guaranteed Amount is borne by all the partners in their profit sharing ratio (Firm Guarantee).

- **When the Guarantee is given by the specific partner: Under the situation where a specific partner provides the Guarantee of Minimum Profit to another Partner, then any deficiency in the Guaranteed Amount is borne by that specific partner only.

- **When a Guarantee of Minimum Profit is given by all the partners in some specific ratio: Any deficiency in the Guaranteed Amount is borne by all the partners in the specific ratio agreed by all the partners (Personal Guarantee).

Steps of Guarantee of Minimum Profit to a Partner

****Step 1:**Determine the firm’s total profit as per the Profit & Loss Account.

**Step 2: Divide the profit among all partners according to the agreed profit-sharing ratio.

****Step 3:**Compare the guaranteed partner’s share with the minimum guaranteed amount.

**Step 4: If the actual share is less than the guaranteed amount:

Deficiency = Guaranteed Amount – Actual Share

**Step 5: The deficiency is borne by the guaranteeing partner(s) in an agreed ratio, or if no ratio is given, then in their profit-sharing ratio.

****Step 6:**Add the deficiency to the guaranteed partner’s share. Deduct the same amount from the guaranteeing partner(s).

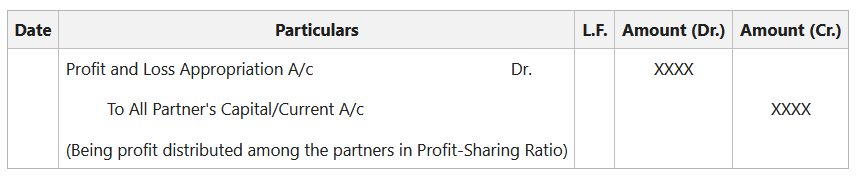

Accounting Treatment (Journal Entries)

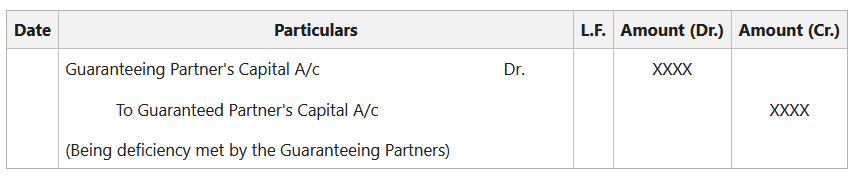

**Case I: When the actual share is less than the guaranteed amount

In this case, the share of deficiency is recovered from the profit share of the Guaranteeing Partners and all the Adjustments are made in the Profit and Loss Appropriation Account before transferring the profit share to the Capital/Current Account of the Partner. The deficient amount is added to the profit share of the Guaranteed Partner in the Profit and Loss Appropriation Account, before transferring it to the Capital/Current Account.

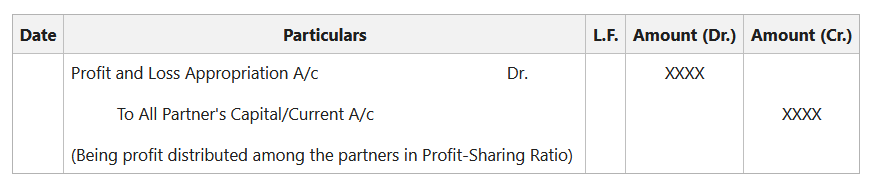

_A. Distribution of Profit/Loss among all the partners as if there is no Guarantee Arrangement:

- **In the case of Profit:

- **In the case of Loss:

_B. Recovering the Share of Deficiency from Guaranteeing Partners:

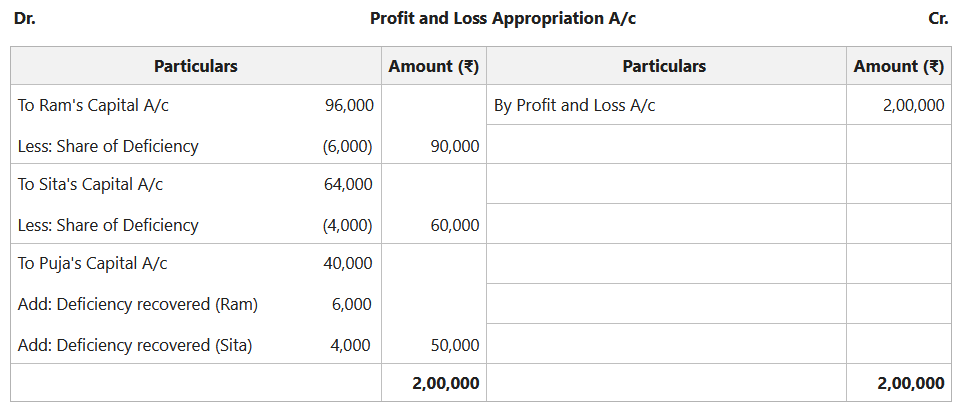

**Example of Guarantee of Minimum Profit to a Partner

Ram, Sita, and Puja are partners sharing profit in the ratio 12:8:5. Puja is being guaranteed that her share of profit shall be a minimum of ₹50,000 p.a. and any deficiency shall be borne by Ram and Sita in their profit-sharing ratio. The Profit for the year ended 31st March 2021 was ₹2,00,000. Pass necessary Journal entries in the book of the firm and prepare the Profit and Loss Appropriation Account.

**Solution:

Puja's Share in the Profit of the firm= 2,00,000\times \frac{5}{25}=₹40,000

Minimum profit guaranteed to her= ₹50,000

Deficiency= 50,000 − 40,000= ₹10,000

**Share of Deficiency of Borne by:

**Ram:

Deficiency Amount payable= 10,000\times \frac{12}{20}=₹6,000

**Sita:

Deficiency Amount payable= 10,000\times \frac{8}{20}=₹4,000

**Distribution of the firm's Profit among the partners as there is no guarantee:

**Ram:

Profit Share= 2,00,000\times \frac{12}{25}=₹96,000

**Sita:

Profit Share= 2,00,000\times \frac{8}{25}=₹64,000

**Puja:

Profit Share= 2,00,000\times \frac{5}{25}=₹40,000

**Case II: When the actual share is more than the guaranteed amount

When the actual profit share of the Guaranteed partner is either equal to or more than the Guaranteed Amount, then under such circumstance no Deficiency arises. So, the profit of the firm is Distributed among the partners as if there is no clause for the guarantee of minimum profit.

_Distribution of Profit among all the partners as if there is no Guarantee Arrangement:

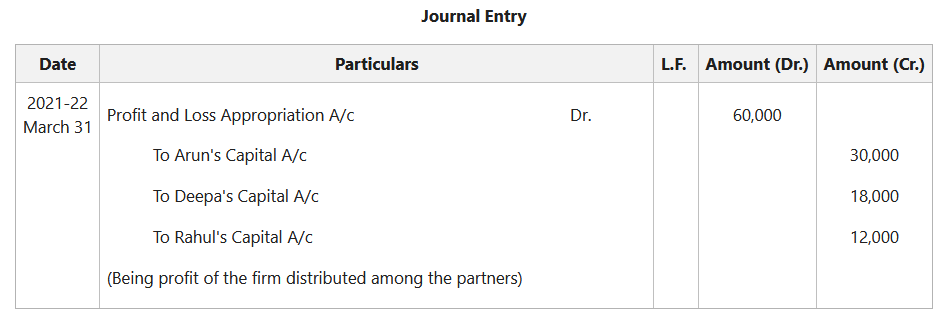

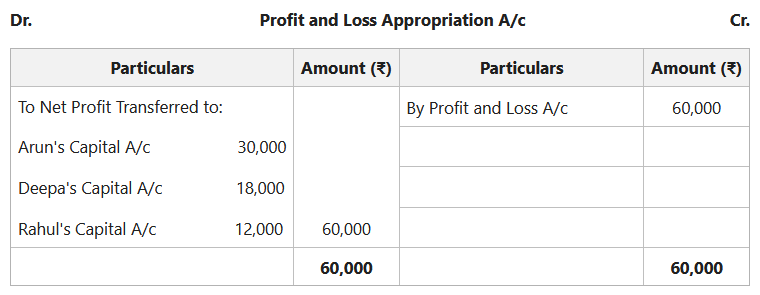

**Illustration:

Arun, Deepa, and Rahul are partners sharing profits in the ratio of 5:3:2. According to the Partnership Agreement, Rahul is to get the minimum amount of ₹10,000 as his share of profit every year. The Net Profit for the year ended 31st March'22 amounted to ₹60,000. Prepare the Profit and Loss Appropriation Account and pass necessary Journal entries in the book of the firm.

**Solution:

**Distribution of Profit among the Partners as if there is no Guarantee:

**Arun:

Profit Share= 60,000\times \frac{5}{10}=₹30,000

**Deepa:

Profit Share= 60,000\times \frac{3}{10}=₹18,000

**Rahul:

Profit Share= 60,000\times \frac{2}{10}=₹12,000