Hidden Goodwill: Admission of a Partner (original) (raw)

Last Updated : 30 Apr, 2026

Goodwill is an intangible asset that shows the value of a business’s reputation and advantages like good location, customer loyalty, and quality service, which help it earn higher profits. It can be self-generated or purchased, but only purchased goodwill is recorded in the books. In a partnership, when a new partner joins, they pay for goodwill to compensate the existing or sacrificing partners for their share of future profits.

Hidden Goodwill:

Hidden goodwill is the value of goodwill that is not directly shown in the books but is calculated indirectly when a new partner is admitted. It is determined by comparing the total value of the firm (based on the new partner’s capital and share) with the actual capital of the firm, and the excess amount is treated as hidden goodwill.

**Calculation of Hidden Goodwill:

**Step 1: Calculate the net worth of the new firm based on the capital brought in by the new partner:

New Firm's Capital = Capital~of~the~new~partner\times Reciprocal~of~share~of~the~new~partner

**Step 2: Calculate the new firm's actual capital by adding the capital of all the partners (including the capital of the new partner).

**Step 3: Calculate the firm's goodwill by deducting the Actual Capital of the Firm (Calculated in Step 2) from the New Firm's Capital (Calculated in Step 1).

**Step 4: Calculate the new partner's share of goodwill:

New partner's share of goodwill = Firm's~Goodwill\times New~Partner's~Share

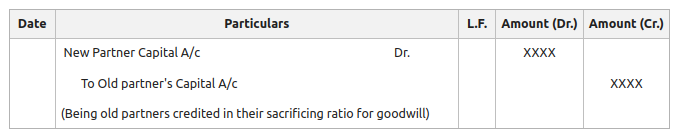

Journal entries passed at the time of admission of the new partner:

**A. For cash brought as a share of capital by the new partner:

**B. For the share of goodwill brought by the new partner adjusted in the old partner's Capital A/c in sacrificing ratio:

**Illustration 1:

M and N are partners in the firm sharing profit and loss in the ratio of 5:3 with the capital of ₹2,05,000 and ₹1,85,000, respectively. P is admitted into the firm as the new partner for 1/5th share in the firm on 1st August 2022. P brings in ₹ 1,90,000 as his share of capital. Give Journal entries on P's admission.

**Solution:

**Working Notes:

**1. Calculation of Hidden Goodwill:

P's Capital = ₹1,90,000 for \frac{1}{5}th share

Total capital of the New Firm = Capital~of~the~new~partner\times Reciprocal~of~share~of~the~new~partner

= ₹1,90,000 x 5

= ₹9,50,000

Total Capital of all the partners = Capital of M + Capital of N + Capital of P

= ₹2,05,000 + ₹1,85,000 + ₹1,90,000

= ₹5,80,000

Goodwill of the Firm = Total capital of firm - Total capital of all partners

= ₹9,50,000 - ₹5,80,000

= ₹3,70,000

P's share of Goodwill = Firm's~Goodwill\times P's~Share~in~Profits

= \frac{1}{5}\times₹3,70,000

= ₹74,000

**2. Calculation of Sacrificing Ratio:

The sacrificing ratio, in this case, will be the old profit sharing of M & N, i.e., **5:3.

**Illustration 2:

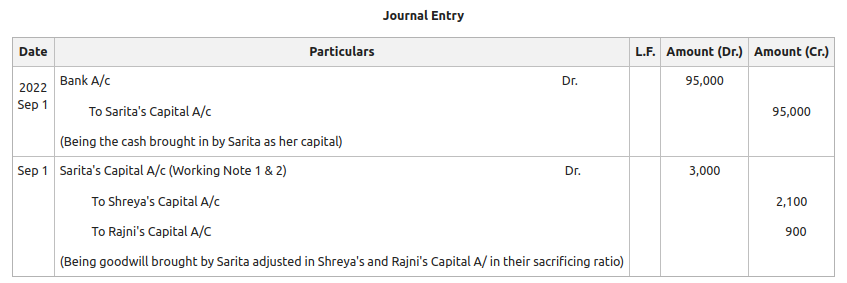

Shreya and Rajni are business partners in the firm sharing profit and loss in the ratio of 6:4 having ₹1,59,000 and ₹1,60,000 as their respective capitals. Sarita is admitted as the new partner in the firm on 1st September 2022, and it was decided that the new profit sharing ratio between Shreya, Rajni, and Sarita will be 8:6:4, respectively. Sarita has to bring ₹95,000 as her share of capital. Pass necessary journal entries.

**Solution:

**Working Notes:

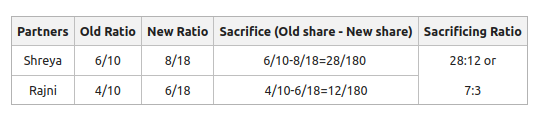

**1. Calculation of Sacrificing Ratio:

**2. Calculation of Hidden Goodwill:

Sarita's Capital =₹95,000 for \frac{4}{18}th share

Total Capital of the New Firm = Capital~of~the~new~partner\times Reciprocal~of~share~of~the~new~partner

= ₹95,000\times\frac{18}{4}

= ₹4,27,500

Total Adjusted Capital of all the partners = Capital of Shreya + Capital of Rajni + Capital of Sarita

= ₹1,59,000 + ₹1,60,000 + ₹95,000

= ₹4,14,000

Goodwill of the Firm = Total capital of firm - Total adjusted capital of all partners

= ₹4,27,500 - ₹4,14,000

= ₹13,500

**Sarita's share in Goodwill = \frac{4}{18}\times₹13,500

**= ₹3,000