Financial Statements : Meaning, Objectives, Types and Format (original) (raw)

Last Updated : 22 Apr, 2026

Financial statements are formal records that present the financial activities and position of a business, organization, or individual. They provide structured information about performance, financial health, and cash movements over a specific period. The financial statements of an organization also help them in different analyses, such as Credit Analysis, Debt Analysis, Security Analysis, and General Business Analysis. To ensure the reliability and accuracy of the financial statements, firms, accountants, government agencies, etc., audits the statements.

**Objectives of Financial Statements

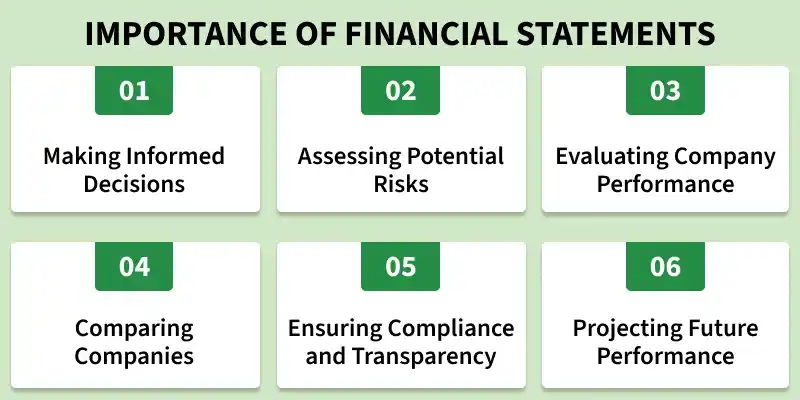

- To provide information about financial performance.

- To show the financial position of the business.

- To assist in decision-making.

- To determine profitability and solvency.

- To evaluate management performance.

**Need for Financial Statements

- Help in financial planning

- Assist in investment decisions

- Support loan approvals

- Measure business performance

- Ensure legal compliance

**Types or Components of Financial Statements

**1. Trading and Profit and Loss Account: it is a financial statement that helps in determining the profit earned or loss incurred by a business during an accounting year. It is prepared to ascertain the operational results of the organization for a specific period. If total revenues exceed total expenses its profit , If total expenses exceed total revenues then its shown as loss. The expenses and losses of the firm are recorded on the debit side of the account, whereas the revenues and profits are recorded on the credit side of the account. Some of the essential items included on the debit side are opening stock, wages, purchases less return, salaries, rent paid, interest paid, commission paid, etc. The items included on the credit side are sales less returns, and other incomes.

**2. Balance Sheet: It is a financial statement of an organization that shows its financial position, liabilities, assets, and stockholder's equity as on the date mentioned in the report. It means that the balance sheet does not show the figures of an organization for an accounting period; instead, it shows the figures on a specific date. There are two sides to a balance sheet, namely, the asset side (on the right side) and the liabilities side (on the left side). The asset side of the balance sheet shows the debit balance of the organization. However, the liabilities side of the balance sheet shows the credit balances. The total of the asset side must always be equal to the total of the liabilities side. The balance sheet of an organization is prepared after the preparation of the Trading and Profit and Loss Account. The balance sheet includes the balances of all those ledger accounts, which have not been transferred to the Trading P&L A/c and are yet to be carried forward to the next financial year of the organization. The relevant items included in the balance sheet of an organization are current liabilities, current assets, capital, fixed assets, investments, drawings, long-term liabilities, etc.

**Format of the Financial Statements

**Trading and Profit and Loss Account

**Note: * or ** represents that the firm will either have gross profit or gross loss, i.e., when credit side is greater than the debit side, the difference is denoted as Gross Profit, and when debit side is more than the credit side, the difference is denoted as Gross Loss. The same will be applied in the case of Net profit and Net loss in Profit and Loss Account.

**Balance Sheet:

**Users of Financial Statements:

- **Investors – Investors use financial statements to evaluate the company’s profitability, growth potential, and level of risk before making investment decisions.

- **Creditors – Creditors examine financial statements to determine the firm’s ability to repay loans and meet interest obligations on time.

- **Management – Management uses financial statements for planning, decision-making, performance evaluation, and controlling business operations.

- **Government – Government authorities review financial statements to assess tax liabilities and ensure compliance with laws and regulations.

- **Employees – Employees refer to financial statements to understand the company’s stability, profitability, and job security prospects.

- **Competitors: Companies competing against each other require financial statements of its competitors so that they can evaluate its performance and financial conditions. It helps them gain knowledge about the firm's competitive strategies and make decisions accordingly.

- **Rating Agencies: Different rating agencies or credit rating agencies use financial statements so that they can review them and give a credit rating to the organization or its securities.

- **Lenders: The lenders use financial statements of the borrower companies to estimate their ability to pay back the loan along with the interest charges.

- **Suppliers: Suppliers to an organization often provide them with the supplies on credit. These suppliers use the financial statements to decide whether or not they should extend the credit to the organization.