Journal Entries under GST (Goods and Services Tax) (original) (raw)

Last Updated : 18 Apr, 2026

Goods and Services Tax (GST) is a single indirect tax that has replaced many indirect taxes in India. It was introduced on 1 July 2017 under the Goods and Services Tax Act. GST is a destination-based tax, which means the tax is collected by the state where the goods or services are finally consumed. GST is charged at every stage of buying and selling goods or services. However, businesses can reduce the tax they have already paid on purchases through a system called Input Tax Credit (ITC).Because of this system, the tax burden finally falls on the ultimate consumer, and businesses only collect and deposit the tax with the government.

The three types of taxes under GST are:

- **Central Goods and Services Tax (CGST): GST levied by the Centre on the Intra-State supply of goods or services i.e supply of goods and services in the same state.

- **State Goods and Services Tax (SGST): GST levied by the State (including Union Territories with legislatures) on the Intra-State supply (supply of goods and services in the same state) of goods or services by the State.

- **Integrated Goods and Services Tax (IGST): GST collected by the Centre and levied on the Inter-State supply of goods or services. In other terms, IGST is the total of CGST and SGST.

Classification of GST for Accounting Purposes:

**1. Input CGST/SGST: Input CGST/SGST is paid on intra-state purchases of goods and services and adjusted against Output CGST/SGST i.e. GST collected on sales.

**2. Input IGST: Input IGST is paid on inter-state purchases of goods and services and adjusted against Output IGST i.e. GST collected on sales.

**3. Output CGST/SGST: Output CGST/SGST is collected on intra-state sales or supply of goods and services.

**4. Output IGST: Input IGST is collected on inter-state sales or supply of goods and services.

The three types of taxes under GST are:

- **Central Goods and Services Tax (CGST): CGST is levied by the Central Government on intra-state supply i.e. supply of goods and services in the same state.

- **State Goods and Services Tax (SGST): SGST is levied by the State Government on intra-state supply i.e. supply of goods and services in the same state.

- **Integrated Goods and Services Tax (IGST): IGST is levied by the Central Government on inter-state supply i.e. Sale between different states.

Example:

- Sale within Maharashtra → CGST + SGST

- Sale from Maharashtra to Gujarat → IGST

Classification of GST for Accounting Purposes:

**1. Input CGST/SGST: Paid on intra-state purchases of goods and services and adjusted against Output CGST/SGST i.e. GST collected on sales.

**2. Input IGST: Input IGST is paid on inter-state purchases of goods and services and adjusted against Output IGST i.e. GST collected on sales.

**3. Output CGST/SGST: Output CGST/SGST is collected on intra-state sales or supply of goods and services.

**4. Output IGST: Input IGST is collected on inter-state sales or supply of goods and services.

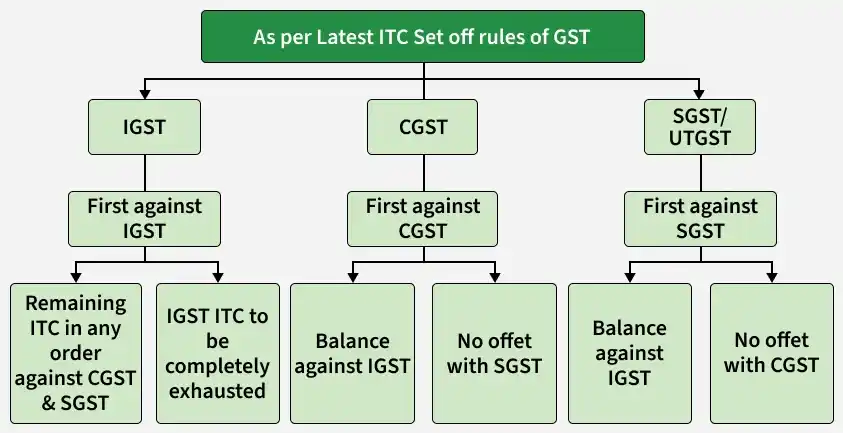

Order of setting off of Input GST:

Journal Entries (In case of Intra-state supply of goods and services i.e. sales within the same state):

**1. For purchase of goods:

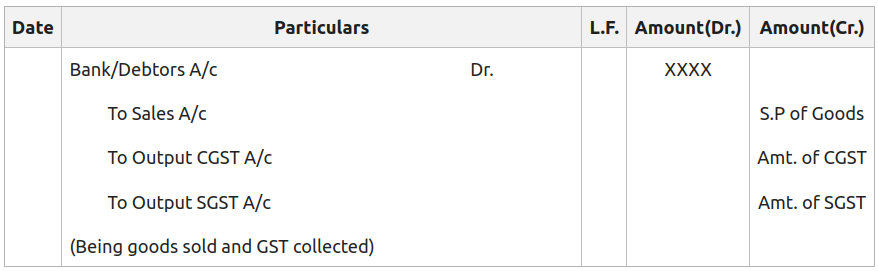

**2. For sale of goods:

**3. For purchase return:

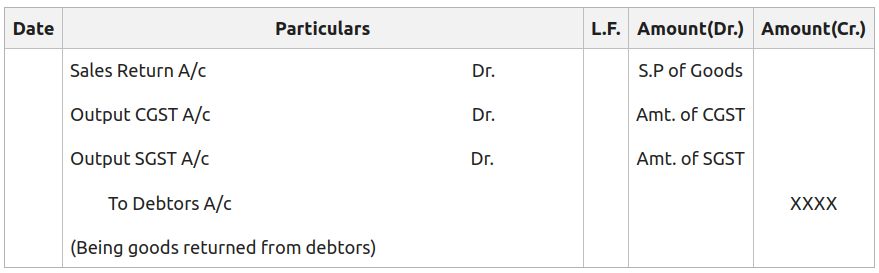

**4. For sales return:

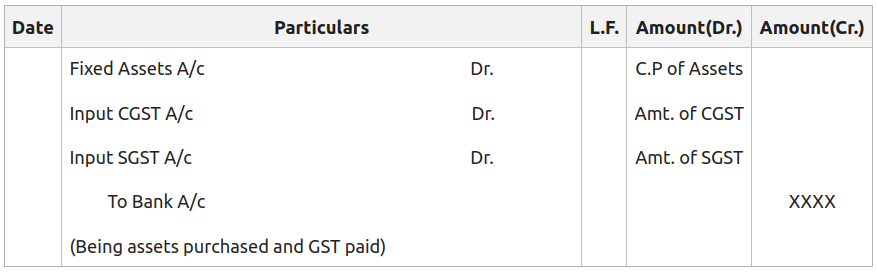

**5. For purchase of fixed assets:

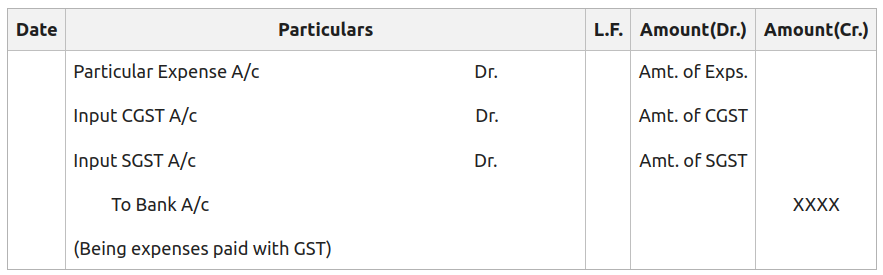

**6. For expenses paid:

**7. For income received:

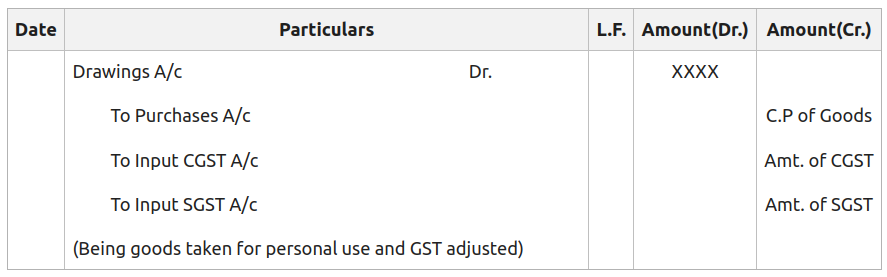

**8. For goods withdrawn by the proprietor for personal use:

**9. For goods given away as free samples/loss of goods by fire/theft:

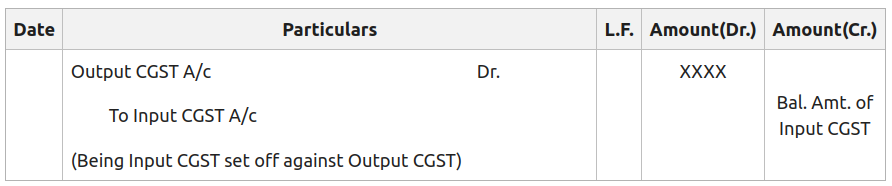

**10. For setting off Input CGST against Output CGST:

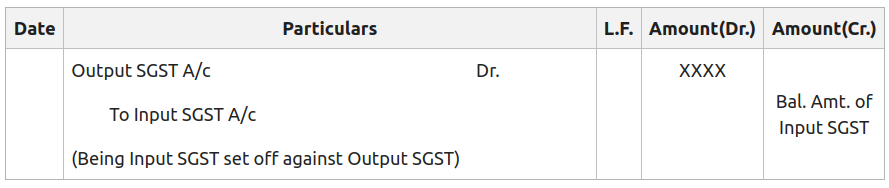

**11. For setting off Input SGST against Output SGST:

**12. For payment of GST:

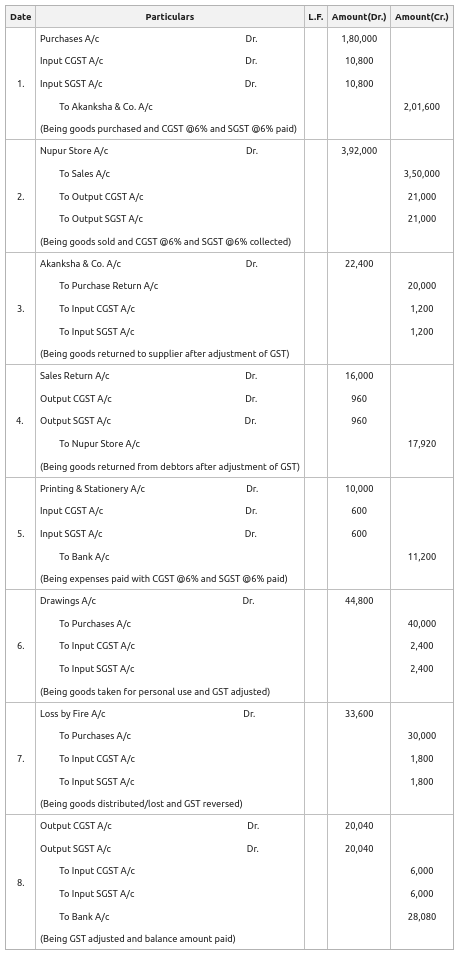

Illustration:

Pass journal entries for the following transactions in the books of Sahil Ltd. assuming that both parties belong to the same state and CGST @6% and SGST @6% are levied:

1. Purchased goods for ₹1,80,000 from Akanksha & Co.

2. Sold goods for ₹3,50,000 to Nupur Store.

3. Returned goods to Akanksha & Co. for ₹20,000.

4. Nupur Store returned goods for ₹16,000.

5. Paid for Printing and Stationary ₹10,000.

6. Goods withdrawn by the proprietor for personal use ₹40,000.

7. Goods destroyed by fire ₹30,000.

8. Payment made of balance of GST.

Solution:

**Working Note:

Total Input CGST = 10,800 - 1,200 + 600 - 1,200 -900 = ₹6,000

Total Input SGST = 10,800 - 1,200 + 600 - 1,200 -900 = ₹6,000

Total Output CGST = 21,000 - 960 = ₹20,040

Total Output SGST = 21,000 - 960 = ₹20,040

Net CGST Paid = 20,040 - 6,000 = 14,040

Net SGST Paid = 20,040 - 6,000 = 14,040

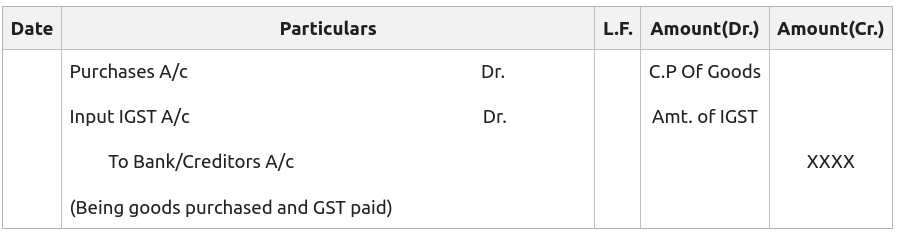

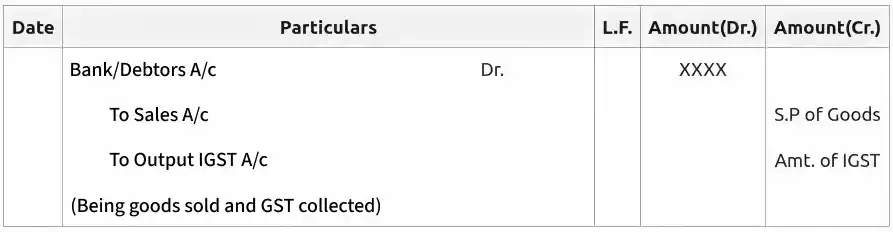

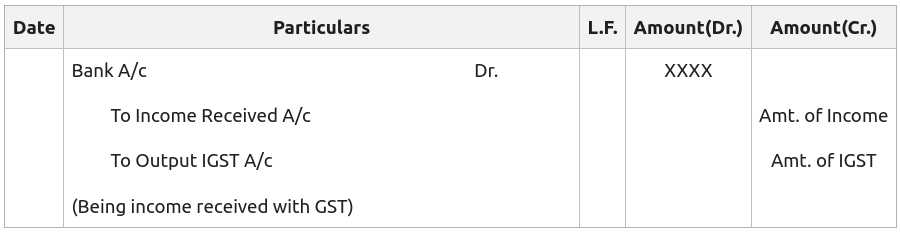

Journal Entries (In case of Inter-state supply of goods and services i.e. sales from one state to another state):

**1. For purchase of goods:

**2. For sale of goods:

**3. For purchase return:

**4. For sales return:

**5. For purchase of fixed assets:

**6. For expenses paid:

**7. For income received:

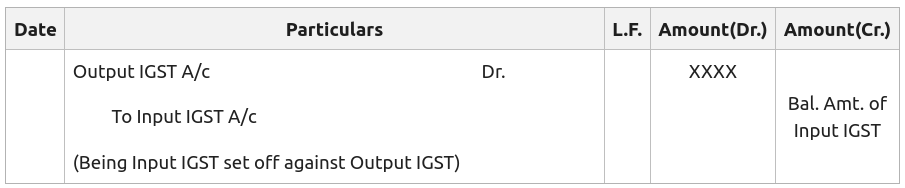

**8. For setting off Input IGST against Output IGST:

**9. If Input IGST exceeds the Output IGST, Input IGST will be first adjusted against CGST, and the balance, if any, will be adjusted against setting off SGST.

Illustration:

Pass journal entries for the following transactions in the books of Sahil Ltd. of Noida, Uttar Pradesh assuming CGST @6% and SGST @6% are levied:

1. Purchased goods for ₹6,00,000 from Sayeba & Co. of Patna, Bihar.

2. Purchased goods for ₹1,00,000 from Gaurav Store of Varanasi, Uttar Pradesh.

3. Sold goods costing ₹1,60,000 to Ishika of Ranchi, Jharkhand at a profit of 25% on cost less 10% Trade Discount.

4. Sold goods costing ₹5,00,000 to Shubham of Allahabad, Uttar Pradesh at a profit of 60% on cost less 15% Trade Discount against cheque which was deposited into the bank.

5. Paid for Advertisement ₹16,000.

6. Purchased a computer for office use for ₹60,000 and payment was made by cheque.

7. Proprietor withdrew ₹20,000 for his personal use.

8. Payment made of the balance amount of GST.

Solution: