Journal Entry for Discount Allowed and Received (original) (raw)

Last Updated : 17 Apr, 2026

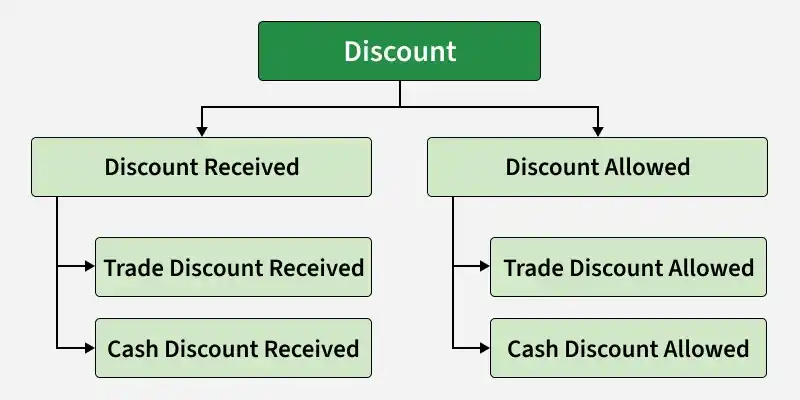

A discount is a concession in the selling price of a product offered by a seller to the customers. According to nature, there are two types of discount:

A. Discount Allowed

B. Discount Received

**A. Discount Allowed: When at the time of sales or receiving cash, any concession is given to the customers, it is called discount allowed.

**Journal Entry:

**Example:

- Goods sold ₹50,000 for cash, discount allowed @ 10%.

- Cash received from Rishabh worth ₹19,500 and discount allowed to him ₹500.

**Solution:

**B. Discount Received: When at the time of purchase or paying cash, any concession is received from the seller, it is called discount received.

**Journal Entry:

**Example:

- Goods purchased for cash ₹20,000, discount received @ 20%.

- Cash paid to Vishal ₹14,750 and discount received from him ₹250.

**Solution:

According to the business point of view, there are two types of Discount:

A. Trade Discount

B. Cash Discount

**A. Trade Discount: The discount provided by the seller to its customers at a fixed percentage on the listed price, mostly on bulk purchases, is called a trade discount. Trade discount is not shown separately in the journal entry.

**Journal Entry:

**Example:

- Goods purchased from Hardik ₹20,000, at less 10% Trade Discount.

- Goods sold to Abhinav for ₹10,000 and offered him a Trade Discount of @5%.

**Solution:

**Example: If goods purchased or sold at a trade discount are returned: (Based on the above example)

- Goods purchased from Hardik worth ₹2,000 were returned.

- Abhinav returned goods worth ₹1,000.

**Solution:

**B. Cash Discount: A Cash discount is offered to those types of customers who make quick payments or payment is made by them within a fixed period.

**Journal Entry:

**Example:

- Goods purchased from Sahil ₹10,000 for cash, at less 10% Trade Discount and 5% cash discount.

- Goods sold to Kashish for ₹20,000 for cash and offered him a Trade Discount @5% and a cash discount @2.5%.

**Solution:

**Notes to Accounts:

**Working Note 1:

**Working Note 2: