Treatment of Special Items in Cash Flow Statement (original) (raw)

Last Updated : 21 Apr, 2025

The movement of cash & cash equivalents or inflow and outflow of cash is known as **Cash Flow. Cash inflows are the transactions that result in an increase in cash & cash equivalents; whereas, cash outflows are the transactions that result in a reduction in cash & cash equivalents. Hence, a statement showing flows of cash & cash equivalent during a specified time period is known as a **Cash Flow Statement. The transactions of a cash flow statement are categorised into three activities; namely, Cash flow from Operating Activities, Cash flow from Investing Activities, and Cash flow from Financing Activities. Besides the main items of the three activities, there are some other special items that are covered under a Cash Flow Statement.

Treatment of Some Other Special Items in Cash Flow Statement:

1. Provision for Taxation:

Accounting Treatment of Income Tax Provision and Income Tax Paid during the year (If it is considered as an Appropriation of Profits):

**Effect:

- **Income Tax Paid: The amount paid will be deducted from the amount of Cash generated from Operations in Operating Activities.

- **Income Tax Provision during the year: The amount of Income Tax Provision during the year will be added in the balance amount of Profit & Loss Appropriation A/c.

**Some Cases:

**Case 1: When only the amount of Income Tax paid during the year is given in the question.

**Solution: In this case, we will assume that the amount of Income Tax Provision during the year is equal to the amount of Income tax Paid during the year.

**Case 2: When only the amount of Income Tax Provision during the year is given in the question.

**Solution: In this case, we will assume that the amount of Income Tax paid during the year is equal to the amount of Income Tax Provision during the year.

**Case 3: When the Opening and Closing Balance of Income Tax Provision is given in the question.

**Solution: In this case, we will assume that:

a) Income Tax Paid = Opening Balance of Income Tax Provision, and

b) Income Tax Provision during the year = Closing Balance of Income Tax Provision

**Illustration:

Provision for Tax (1st April 2020) = ₹2,00,000

Provision for Tax (31st March 2021) = ₹2,50,000

**Solution:

Income Tax Paid = ₹2,00,000

Income Tax Provision during the year = ₹2,50,000

**Case 4: When the Opening and Closing Balance of Income Tax Provision is given along with Income Tax Paid/Provision for Income Tax.

**Solution: In this case, we will assume that:

a) Income Tax Paid = Opening Balance of Income Tax Provision + Provision for Income Tax during the year - Closing Balance of Income Tax Provision

b) Income Tax Provision = Closing Balance of Income Tax Provision + Income Tax Paid - Opening Balance of Income Tax Provision

**Illustration:

Provision for Tax (1st April 2020) = ₹1,00,000

Provision for Tax (31st March 2021) = ₹1,40,000

**Additional Information: Income Tax paid during the year ₹80,000.

Find out the Provision for Tax made during the year.

**Solution:

Income Tax Provision = ₹1,40,000 + ₹80,000 - ₹1,00,000

= ₹1,20,000

2. Provision for Dividend:

Accounting Treatment of Provision for Dividend and Dividend Paid during the year (If it is considered as an Appropriation of Profits):

**Effect:

- **Dividend Paid: The amount of Dividend Paid is deducted from Financing Activities.

- **Provision for Dividend during the year: The amount of provision for dividend during the year is added to the Balance amount of Profit & Loss Appropriation A/c.

Some Cases:

**Case 1: When only the amount of Dividend Paid during the year is given in the question.

**Case 2: When only the amount of Provision for Dividend during the year is given.

**Solution: In the above two cases, we will assume that the amount of Dividend Paid during the year is equal to the amount of the Provision for Dividend during the year.

**Case 3: When the Opening and Closing Balance of Provision for Dividend is given.

**Solution: In this case, we will assume that:

a) Dividend Paid = Opening Balance of Provision for Dividend, and

b) Provision for Dividend during the year = Closing Balance of Provision for Dividend.

**Illustration:

Provision for Dividend (1st April 2020) = ₹60,000

Provision for Dividend (31st March 2021) = ₹1,00,000

**Solution:

Dividend Paid = ₹60,000

Provision for Dividend during the year = ₹1,00,000

**Case 4: When the Opening and Closing Balance of Provision for Dividend is given along with the Provision for Dividend/Dividend Paid.

**Solution: In this case, we will assume that:

a) Dividend paid = Opening Balance of Provision for Dividend + Provision for Dividend during the year - Closing Balance of Provision for Dividend

b) Provision for Dividend = Closing Balance of Provision for Dividend + Dividend Paid - Opening Balance of Provision for Dividend

**Illustration:

Provision for Dividend (1st April 2020) = ₹80,000

Provision for Dividend (31st March 2021) = ₹1,20,000

**Additional Information: Dividend paid during the year ₹50,000.

Find out the Provision for Dividend made during the year.

**Solution:

Provision for Dividend = ₹1,20,000 + ₹50,000 - ₹80,000

= ₹90,000

It means issue of new share capital (either preference or equity). Issue of shares is a source of cash for a company, as it helps in the flow of cash. However, sometimes a company may issue shares for consideration other than cash. There are three such cases for issue of shares for consideration other than cash:

- The issue of shares or making partly paid shares as fully paid out of the accumulated profits in the form of bonus shares is not a source of cash.

- Issue of Shares for considerations other than current assets, for example, against purchase of land, machines, etc., does not amount to inflow of cash.

- Conversion of Debentures or loans into shares also does not amount to inflow of cash.

In the three cases mentioned above, the accounts involved are non-current and not current assets of funds. Therefore, in any of the above three cases, there will be no effect on the Cash Flow Statement.

**Illustration:

**Additional Information: Equity shares were issued during the year against the purchase of machinery and stock for ₹40,000 and ₹30,000 respectively.

**Solution:

**Treatment:

- Issue of share capital against Machinery is neither an application of cash nor a source of cash, as the nature of both Machinery A/c and Share Capital A/c is non-current. Therefore, there will be no entry for this in a Cash Flow Statement.

- Issue of shares against Stock is a source of cash for the company; hence, it will be shown in Investing Activities.

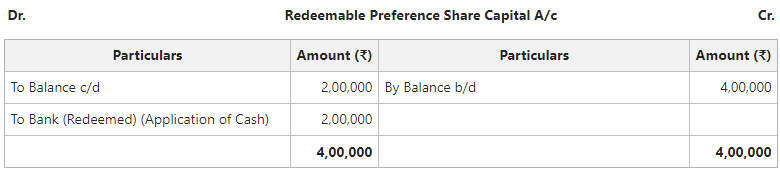

4. Redemption of Preference Shares:

A company can redeem only those Preference Shares which are redeemable as per the terms and conditions specified at the time of issue of these shares. A company can redeem Preference Shares in the following manner:

**a) At Par: When Preference Shares are redeemed at par, in such case the amount of shares will be deducted from Cash Flow from Financing Activities.

**Illustration:

**Additional Information: 8% Preference Shares were redeemed at par. Prepare necessary Accounts to show application of cash.

**Solution:

**b) At Premium: When Preference Shares are redeemed at Premium, in that case, the excess amount of premium paid along with the face value of the shares will be treated as a charge to Profit & Loss A/c. Also, the amount paid to preference shareholders (including premium) will be treated as an application of cash and will be included in Financing Activities.

**Illustration:

**Additional Information: 8% Preference Shares were redeemed at 6% premium. Prepare necessary Accounts to show an application of cash.

**Solution:

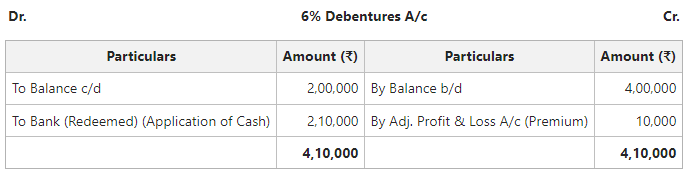

5. Redemption of Debentures:

Debentures of a company can be redeemed at Par and Premium. The amount of Premium at the time of redemption is charged from Profit & Loss A/c and the amount paid will be shown as an application in the cash flow statement under Financing Activities. However, a company may sometimes redeem the debentures by conversion or through the purchase of its own debentures from the market at a lower rate. In the former case, there will be no flow cash; hence, no effect on the cash flow statement. However, in the latter case, the amount of Profit on redemption will be shown on the credit side of Adjusted Profit & Loss A/c.

**Illustration:

Find the amount of redemption for the purpose of Cash Flow Statement if the debentures are redeemed at 5% Premium.

**Solution: