Theory of Supply (original) (raw)

Last Updated : 15 Jan, 2026

Supply refers to the quantity of a commodity that producers are willing and able to offer for sale at various prices during a given period of time. It represents the seller’s side of the market and reflects how producers respond to changes in market conditions.

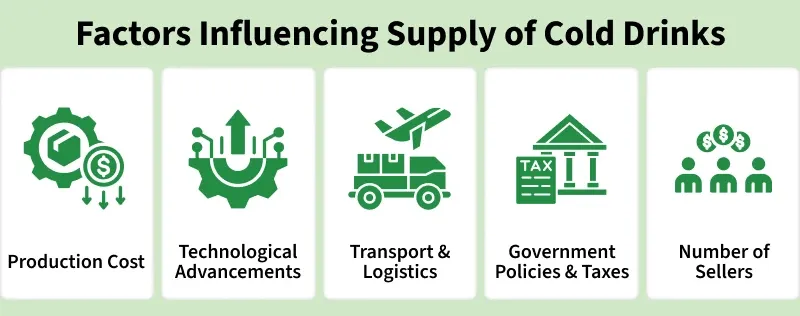

Several economic factors influence supply. These include the cost of production, availability of factors of production, technology, and government policies such as taxes and subsidies. Favorable conditions like lower production costs, technological improvements, or subsidies tend to increase supply, whereas higher costs, restrictive regulations, or heavy taxation can reduce the supply of goods.

Along with demand, supply plays a crucial role in determining the equilibrium price and quantity in the market. The interaction between supply and demand ensures that prices adjust until the quantity supplied equals the quantity demanded, thereby maintaining market balance.

Supply and Stock

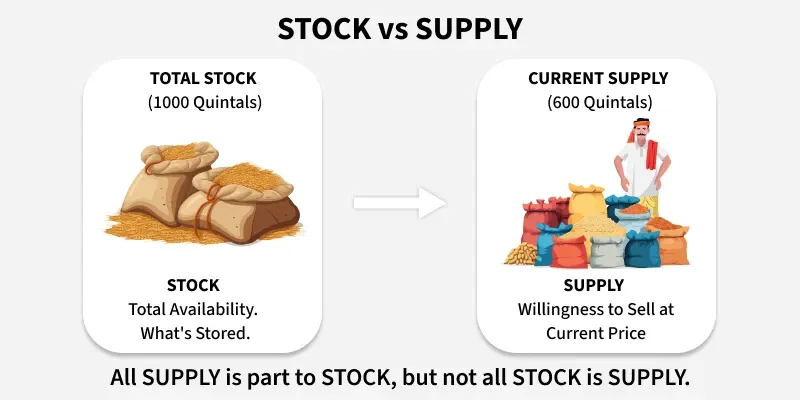

It is important to understand that supply is not the same as the total quantity of goods available. Many people assume that whatever a producer possesses in stock is also supplied in the market, but this is not true.

- Stock refers to the total quantity of a good that a producer or firm has at a given point in time, whether or not it is ready for sale.

- Supply, on the other hand, is that part of the stock that the producer is willing and able to offer for sale at a particular price and during a given period.

Stock is overall quantity, supply is current offering.

A wheat dealer may have 1,000 quintals of wheat stored, but he may decide to sell only 600 quintals at the current price. The total stock is 1,000 quintals, but the supply is only 600. The rest may be kept for future sale if prices rise. Hence, all supply is a part of stock, but all stock is not supply. Stock represents total availability, while supply reflects willingness to sell.

This distinction also highlights that supply is a flow concept measured over a period, whereas stock is a static concept measured at a particular moment. Understanding this helps explain why producers may withhold goods at times of low prices and release them when market prices improve, thereby influencing total supply.

The law of supply is based on this idea. It states that, other things remaining constant, the quantity supplied of a commodity increases with a rise in its price and decreases with a fall in price. This happens because higher prices mean higher potential profits, which encourage producers to expand output and sales.

**Individual and Market Supply

The concept of supply can be studied at two levels: individual supply and market supply.

- Individual supply refers to the quantity of a commodity that a single producer or seller is willing to offer for sale at various prices during a specific period. It depends on factors such as production cost, available resources, and expected future prices.

- Market supply represents the total quantity of a commodity that all producers in the market are willing to offer for sale at different prices during a given period. It is obtained by horizontally adding the individual supply schedules of all producers in the market. Hence, market supply reflects the collective behavior of all firms.

While both follow the same principles, the scope of market supply is wider. It considers not only the price of the commodity but also industry-wide factors like the number of producers, market conditions, and government policies.

**Characteristics of Supply

**Dependence on Price

Supply is directly related to the price of the commodity. When the price rises, producers are encouraged to supply more since higher prices increase profits. Conversely, when the price falls, producers may hold back a part of their stock, reducing the quantity supplied.

**Defined Time Period

Supply always refers to a specific time period such as a day, month, or year because production and sale decisions cannot be changed instantly. The time element is important, as firms need time to adjust output in response to price changes.

**Influence of Productive Capacity

The amount that can be supplied depends on the productive capacity of the firm. Limited machinery, labor, or raw materials can restrict output, even when prices are high. Thus, supply is constrained by available resources and production capacity.

**Aggregation in Market Supply

Market supply is the total of all individual supplies in the market. It reflects the total quantity of a good that producers are willing to sell collectively at different price levels.

**Effect of Expectations

Expectations about future prices strongly affect supply. If producers anticipate higher prices later, they may restrict current sales to gain higher returns in the future. Conversely, if prices are expected to fall, producers might increase supply now to avoid losses.

**Relation with Cost of Production

Cost of production directly affects the ability and willingness to supply. When production costs increase, profits shrink, causing supply to contract. When costs fall due to efficiency or cheaper inputs, supply expands as producers find it profitable to produce and sell more.

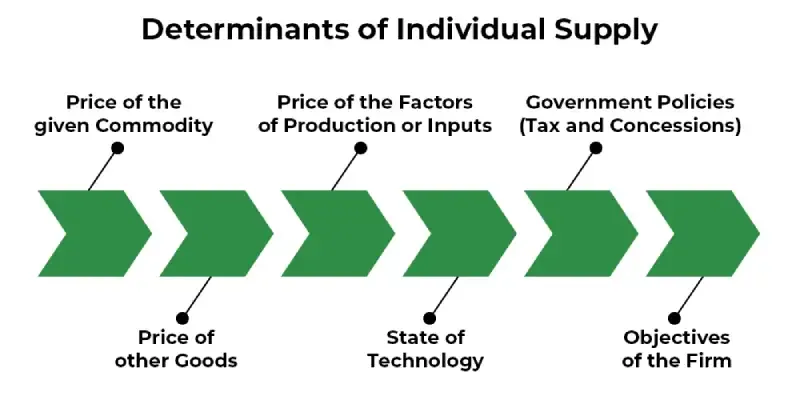

**Determinants of Individual Supply

Individual supply refers to the quantity of a commodity that a single producer is willing and able to offer for sale at different prices during a given period of time. The supply decision of an individual producer is influenced by several factors.

**Price of the Given Commodity

The most basic factor affecting supply is the commodity’s own price. When the price of a good rises, producers find it more profitable to sell and therefore increase the quantity supplied. On the other hand, when the price falls, producers may prefer to hold back their goods or produce less, reducing supply. This positive relationship between price and quantity supplied forms the foundation of the law of supply.

**Price of Other Goods

The prices of other goods influence how producers allocate their resources among different products. If the price of a substitute product increases, producers may shift their resources to produce more of that good and reduce the supply of the existing one. For example, if the price of cotton increases, a farmer might shift land from wheat cultivation to cotton farming, leading to a decrease in the supply of wheat.

**Price of the Factors of Production or Inputs

Inputs like labor, machinery, raw materials, fuel, and electricity play a key role in determining production cost. When the prices of these factors rise, the cost of production increases, making it less profitable to supply the same quantity at existing prices. As a result, supply decreases. Conversely, when input prices fall, production becomes cheaper and more profitable, encouraging firms to expand supply.

**State of Technology

Technology determines the efficiency of production. Improved methods, machinery, and processes allow producers to produce more output with the same amount of inputs, reducing cost per unit. As technology advances, productivity rises and the overall supply in the market increases. Outdated technology, on the other hand, limits output and keeps supply low.

**Government Policies (Tax and Concessions)

Government policies such as taxes, subsidies, and concessions strongly influence supply. When the government imposes higher taxes on production, the cost of production rises, discouraging producers from supplying more. In contrast, subsidies or tax concessions reduce costs and motivate producers to increase supply. Hence, favorable government policies promote supply, while restrictive ones reduce it.

**Objectives of the Firm

The goals and motives of a firm also affect its supply decisions. A firm focused on profit maximization may restrict output to maintain higher prices, whereas a firm aiming for sales growth or market expansion might increase supply even with lower profits. Thus, supply decisions depend not only on price and cost but also on the firm’s overall business strategy.

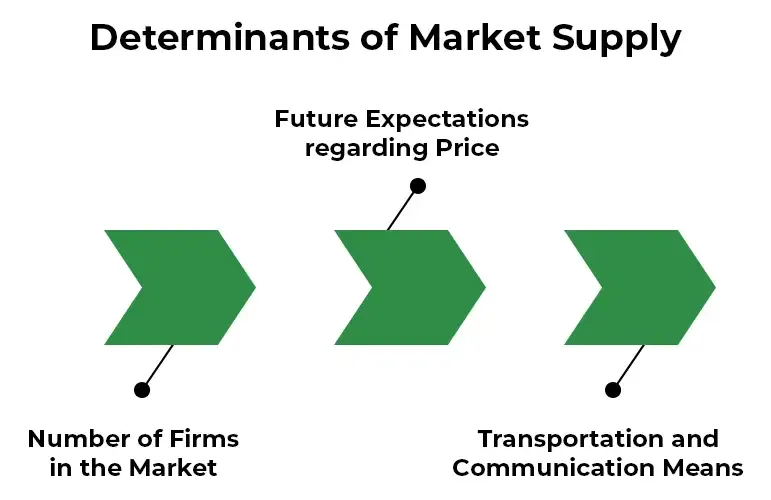

**Determinants of Market Supply

Market supply is influenced by various economic and non economic factors that affect the ability and willingness of producers to offer goods for sale. Changes in these factors can lead to an increase or decrease in the overall supply available in the market.

**Number of Firms in the Market

The total number of firms producing a particular good directly affects the overall market supply. When more firms enter the industry, the total output available in the market increases. Conversely, if firms shut down or exit due to losses or competition, total supply decreases. Hence, the size and structure of the industry determine the level of market supply.

**Future Expectations Regarding Price

Producers’ expectations about future price changes significantly influence how much they supply today. If producers expect prices to rise in the near future, they may hold back part of their output to sell later at higher prices, leading to a temporary fall in current supply. On the other hand, if they expect prices to decline, they may increase present supply to avoid potential losses.

**Transportation and Communication Means

Efficient and modern means of transport and communication make it easier to move goods from production centers to markets quickly and at lower cost. Improved infrastructure reduces wastage and delays, thereby increasing market supply. In contrast, poor transport or communication facilities limit how much producers can sell, even if they have produced enough goods.