statsmodels.expected_robust_kurtosis() in Python (original) (raw)

Last Updated : 10 May, 2020

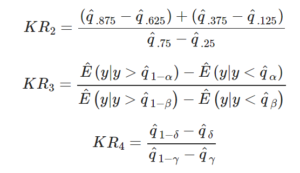

With the help of **statsmodels.expected_robust_kurtosis()** method, we can calculate the expected value of robust kurtosis measure by using statsmodels.expected_robust_kurtosis() method.

Syntax :

statsmodels.expected_robust_kurtosis(ab, db)Return : Return the four kurtosis value i.e kr1, kr2, kr3 and kr4.

**Example #1 :**In this example we can see that by using statsmodels.expected_robust_kurtosis() method, we are able to get the expected value of robust kurtosis measure by using this method.

Python3 1=1 `

import numpy and statsmodels

import numpy as np from statsmodels.stats.stattools import expected_robust_kurtosis

Using statsmodels.expected_robust_kurtosis() method

gfg = expected_robust_kurtosis()

print(gfg)

`

Output :

[3.0000000 1.23309512 2.58522712 2.90584695]

Example #2 :

Python3 1=1 `

import numpy and statsmodels

import numpy as np from statsmodels.stats.stattools import expected_robust_kurtosis

Using statsmodels.expected_robust_kurtosis() method

gfg = expected_robust_kurtosis([12, 22], [6, 7])

print(gfg)

`

Output :

[3.0000000 1.23309512 1.23859789 1.0535188 ]