Accounting Voucher: Format & Types of Vouchers (original) (raw)

Last Updated : 15 Apr, 2026

In a business, there are numerous transactions that take place on regular basis, these can be the purchase , sale , receiving or paying cash, and many more. Transaction basically refers to any monetary activity that affects the financial statements and is documented as an entry in the books of accounts. It involves any kind of exchange involving money, goods, or services. But for every financial transaction taking place in business, there should be valid documentary evidence that supports each transaction. This documentary evidence supporting transactions is known as 'Source documents'. Common examples of source documents are cash receipts, cheques, pay-in-slip, invoices, etc.

Accounting Voucher

Vouchers are prepared to support the accounting entries made in the books of accounts to provide correctness to the transactions. For every business firm or party involved, there are vouchers in the name of every firm with their specific name. Also, different vouchers are created for every transaction as well. Every voucher indicates the accounts that are required to be credited or debited. For every voucher, there is a certain serial number written on it and its related source document. The main reason to assign a serial number to every voucher is to make it easy for the auditors to file and vouch them.

Source Documents

Source documents are original and authentic records of business transactions. They contain important details such as the name of the party, date, amount, and nature of the transaction. These documents form the basis for recording entries in the books of accounts. Each source document usually carries a unique number for identification. They provide documentary evidence as per the principle of verifiability and help auditors in auditing and tax assessment. On the basis of source documents, vouchers are prepared to record transactions systematically.

Difference between Voucher and Source Documents

| Voucher | Source Documents |

|---|---|

| 1. Vouchers denote the evidence of the transaction. | 1. Source document refers to the document recording transactions in the correct manner. |

| 2. Vouchers are supported by the source documents. | 2. Source document provides the base to prepare the vouchers. |

| 3. Vouchers contain information on what account is to be debited or credited. | 3. Source document only collects the details of the business transactions. |

| 4. The main purpose of preparing vouchers is not to record transactions and rather to verify transactions. | 4. The main purpose of preparing the source documents is to record business transactions. |

| 5. Common Examples of Vouchers are: debit note, credit note, letter of credit, etc. | 5. Common examples of source documents are cash memos, invoices or bills, cash receipts, etc. |

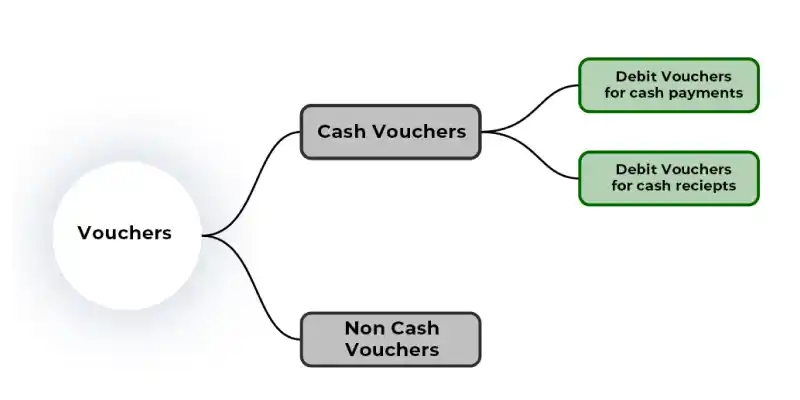

Types of Vouchers

A. Cash Voucher

Cash Vouchers basically refer to vouchers that incorporate all the cash transactions that are cash receipts and payments. Under the category of Cash vouchers, there can be two types of vouchers; Debit Vouchers and Credit Vouchers.

**1. Debit Vouchers:

Debit Vouchers are prepared to record transactions related to the cash payments like:

- Cash payments to buy goods

- Cash payments to buy fixed assets & investments

- Cash payments to Creditors

- Cash payments regarding expenses (rent, salaries, etc.)

- Securing cash in the banks

Details included in the Debit Voucher:

- Date on which transaction is recorded

- Serial no. of Voucher

- Name of the account debited

- Amount involved in the debit transaction

- Description of the transaction along with required information.

- Serial Number of the Source document attached to the Voucher

**2. Credit Vouchers:

Credit Vouchers are prepared to record the transactions relating to the cash receipts like:

- Cash receipts from selling goods

- Cash receipts from selling out fixed assets & investments

- Cash receipts from debtors

- Cash receipt related to income (interest income etc.)

- Withdrawal of cash from the banks.

Details included in the Credit Voucher:

- Date on which transaction is recorded

- Serial no. of Voucher

- Name of the account credited

- Amount involved in the credit transaction

- Description of the transaction along with required information

- Serial Number of the Source document attached to the Voucher

B. Non-Cash Vouchers

Non-cash vouchers are also known as Transfer Vouchers. These vouchers basically incorporate all the non-cash transactions. Following are the details scribbled in the Non-cash voucher.

Details included in the Non-cash voucher:

- Buying or Selling goods on credit

- Buying or Selling out fixed assets & investments

- Goods sold on credit

- Returns of goods bought

- For writing off bad debts

- To provide depreciation

Details included in the Non-Cash Voucher:

- Date on which Voucher is prepared

- Serial no. of Voucher

- Name of the account debited or credited in regard to credit transactions

- Amount involved in the credit transactions

- Description of the credit transaction along with required information

- Serial number of Source document attached to the particular voucher

Illustration:

There is a business named M/s Shikha Enterprises (59/3 Model Town, New Delhi, 110006). On April 14, 2022, this business purchased 5 wooden chairs at the unit price of ₹500 each and 10 plastic chairs at the unit price of ₹300 each on credit from The Furniture Hub. Prepare a voucher for this particular transaction:

Solution:

Format of Voucher

Advantages:

- **Accuracy: Accounting vouchers help ensure the accuracy of financial records, as they provide a detailed record of each transaction.

- **Proper Record Keeping: Accounting vouchers help to keep proper financial records by providing a structured format for recording transactions.

- **Audit trail: Auditors can easily verify transactions because vouchers contain detailed information.

- **Accountability: Accounting vouchers help ensure accountability by documenting who authorized and carried out each transaction.

- **Compliance: Accounting vouchers help businesses comply with tax and regulatory requirements by providing detailed records of financial transactions.

- **Prevents Fraud: Since vouchers require authorization and supporting documents, they reduce the risk of fraud and unauthorized payments.

**Disadvantages:

- **Time-consuming: Creating and managing accounting vouchers can be time-consuming, especially for businesses with a large volume of transactions.

- **Paperwork: Accounting vouchers can result in a significant amount of paperwork, which can be difficult to manage and store.

- **Complexity: Accounting vouchers can be complex, especially for businesses with multiple accounts or subsidiaries, leading to potential errors and confusion.

- **Cost: Accounting vouchers may require additional resources and software, leading to additional costs for businesses.

- **Vulnerability: Accounting vouchers are vulnerable to loss, theft, or damage, which can impact the accuracy and completeness of financial records.