Introduction to Accounting (original) (raw)

Last Updated : 2 May, 2026

The American Institute of Certified Public Accountants(AICPA) defines Accounting as the art of recording, classifying, and summarizing the transactions and events that are in monetary terms efficiently and effectively and interpreting the results.

The main aim of accounting is to ascertain the profit or loss and determine the financial position of an organization so that the firm can communicate the same with the interested parties or users of Accounting Information. The nature of Accounting is dynamic and analytical and hence, requires special abilities and skills in an individual to interpret the information better and effectively.

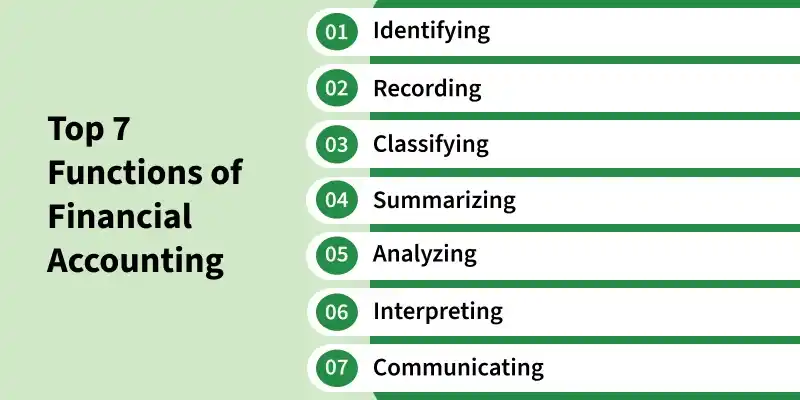

Functions of Accounting

**Identifying-Recognizing and selecting financial transactions and events that should be recorded in the books of accounts.

**Recording – Systematically documenting financial transactions in chronological order in the books of accounts.

**Classifying – Grouping recorded transactions into appropriate ledger accounts to organize financial data.

**Summarizing – Compiling classified data into financial statements like the income statement and balance sheet.

**Analysing – Evaluating financial information to assess performance, profitability, and financial position.

**Interpreting – Explaining the meaning and implications of financial results to aid decision-making.

**Communicating – Presenting financial information clearly to stakeholders such as investors, managers, and creditors.

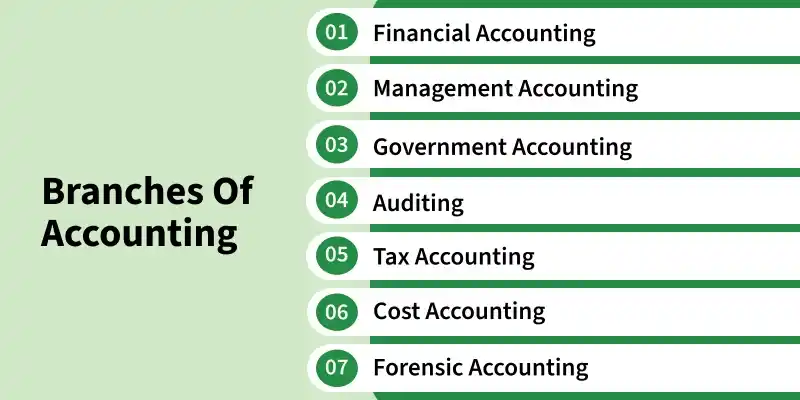

Branches of Accounting

- **Financial Accounting – Records transactions and prepares financial statements for external users like investors and creditors.

- **Cost Accounting – Determines and controls the cost of production to improve efficiency and reduce expenses.

- **Management Accounting – Provides information to management for planning, decision-making, and performance evaluation.

- **Tax Accounting – Handles tax calculations, tax return preparation, and compliance with tax laws.

- **Auditing – Examines financial records to ensure accuracy and compliance with accounting standards.

- **Government Accounting – Manages financial records of government organizations and ensures proper use of public funds.

- **Forensic Accounting – Investigates financial fraud and disputes using accounting, auditing, and investigative skills.

**Accounting Information

It is defined as the information provided by an organization in its financial statements for different internal and external users. An organization prepares the accounting information with the help of the Book-keeping process. The process helps the different users in understanding the financial position and profitability of the organization and make financial decisions accordingly.

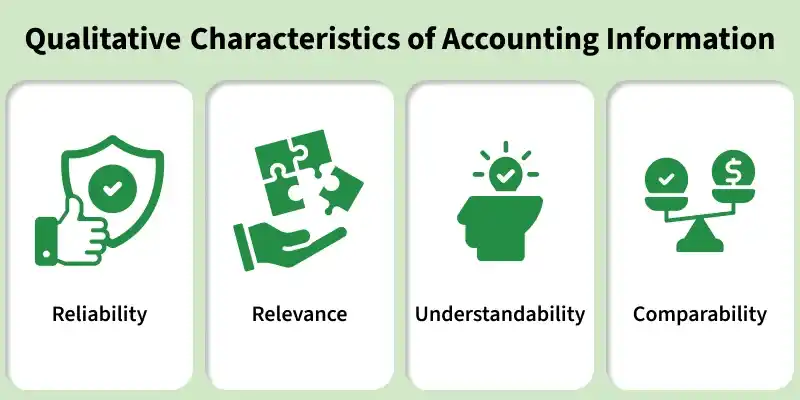

**Qualitative Characteristics of Accounting Information

- **Reliability: It is the ability of a user to depend on the information provided by an organization. Accounting information can be stated as reliable if it is free from errors any kind of personal bias. In other words, the information provided by an organization must be verifiable and based on proper facts.

- **Relevance: It is the ability of information to meet the users' needs and help them make important decisions. The information provided by the organization must be available to the users on time and hence, help them in forecasting.

- **Understandability: It means presenting the accounting information of an organization in a way that the users can understand it in the same sense as the organization wants to convey. With proper understandability only, an organization can communicate effectively with the different users of accounting information.

- **Comparability: Relevance and Reliability of the accounting information is not enough; it should also be comparable. It means that the organization should use the same measures of reporting and accounting principles, so the users can effectively compare the current year's reports with the previous years'.

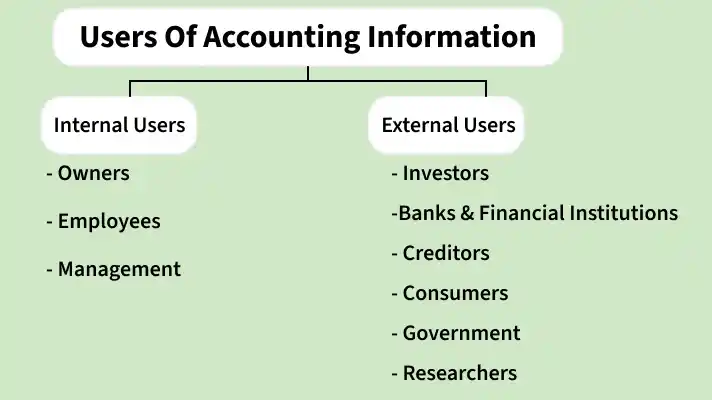

**Users of Accounting Information

Users of accounting information are the people or groups who use financial information to make decisions about related with the organisation. They are mainly classified into internal users and external users.

**1. Internal Users

- **Owners: The owners contribute their savings as capital in the business. So ,they want to know financial position of the organisation.

- **Employees: The employees are interested in the accounting information to know job security , bonuses and salary.

- **Management: The management wants to know accounting information for planning, decision-making, and controlling business activities.

**2. External Users

- **Investors: Investors are the individual or groups of people who invest their money in organizations. These investors want to know about the earning capacity of the organization so they can decide the safety and risk level of investing in an organization.

- **Banks and Financial Institutions: The banks and financial institutions provide loans to different businesses. They use the accounting information to ensure the repayment of their loan.

- **Creditors: Creditors provide goods on credit. They take the help of accounting information to understand the credibility and financial soundness of the organization to pay their money.

- **Consumers: Consumers use the accounting information to know reliability and efficiency of the business.

- **Government: The Government uses accounting information to determine and assess the tax liability of an organization.

- **Researchers: Researchers use the accounting information of an organization to complete their research work and provide actual facts and figures in their work.