Accounting Standards (original) (raw)

Last Updated : 20 Feb, 2026

Formal guidelines and rules that dictate how companies must recognize, measure, present, and disclose financial transactions in their financial statements. They ensure consistency, transparency, and comparability of financial information, which helps investors, regulators, and other stakeholders make informed decisions.

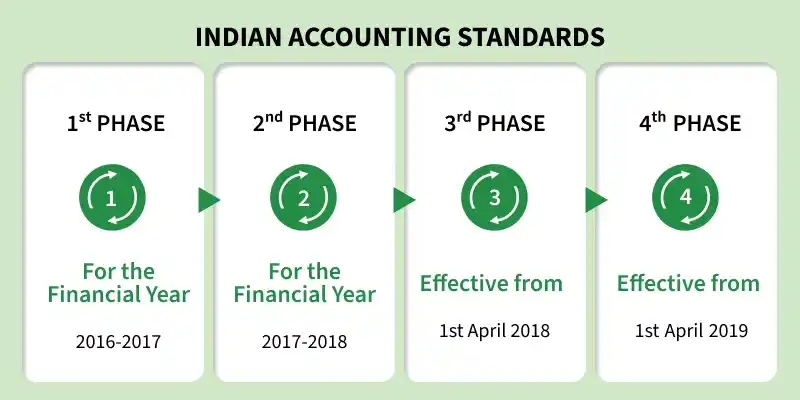

Indian Accounting Standards

Indian Accounting Standards, commonly referred to as Ind AS, are the accounting rules followed by certain companies in India. The Institute of Chartered Accountants of India (ICAI) establishes the standards to be followed in India, and these standards were established under the oversight of the Accounting Standards Board. These standards ensure uniformity, transparency, consistency, and comparability across firms.

Need for Accounting Standards

Accounting Standards are needed due to the following reasons:

- These standards ensure uniformity in financial statements across the firms so that the investors can understand them easily and clearly, and can take appropriate decisions about the investment.

- If the same accounting standards are followed throughout the world, anyone can explore career opportunities in accounting in any part of the world. This facilitates international trade, investment, and cross-border transactions

- It increases transparency by requiring proper disclosure of accounting policies and financial information.

- Ind AS ensures better comparability of financial statements between different companies and across different accounting periods. As everyone following the same guidelines.

- It supports compliance with legal and regulatory requirements and promotes better corporate governance.

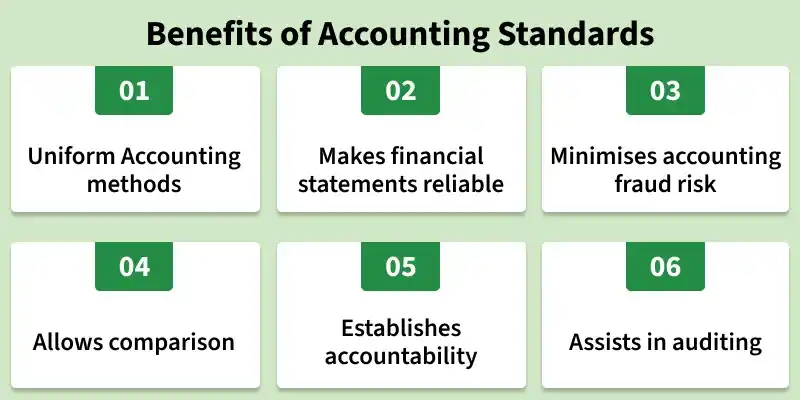

Benefits of Accounting Standards

**1. Reduces Fraud risk : If certain standards are followed during the creation of financial reports, then it can reduce confusion due to multiple people creating the reports in their own way but by following same rules.it also minimise the risk of accounting fraud

**2. Comparability: Accounting Standards ensure that the reports of any organisation can be compared with that of others across the globe.

**3. Uniformity: Each transaction can be easily identified with the use of Accounting standards, as a particular type of transaction will follow certain rules and standards to record it in the reports and statements.

**4. Reliability: Financial Statements and Reports that follow accounting standards allow stakeholders to take important decisions regarding investment easily as this ensure that the financial reports and statements of an organisation are fair and transparent .

Limitations of Accounting Standards

**1. Lack of Flexibility: In accounting, there are many alternatives for valuations. It becomes very difficult to use different valuation methods to create reports, as a particular method can only be followed at a particular time instead of multiple methods, which may make the valuations lengthy and difficult.

**2. Difficulty for Management: It is complex and difficult to understand especially for small businesses as it involves so many rules, methods and guidelines for accounting.

**3. Restricted Scope: Accounting Standards cannot override the statute and needs to be framed within the boundaries of the law that is applicable at that time.

Applicability of Accounting Standards

For accounting standards to be applicable to various organisations, all enterprises are classified into three categories that are Level I, Level II and Level III. Certain accounting standards may not be applicable to a particular level. Let us see the list of accounting standards, and to which level they are applicable.

- **Level I: Companies whose equity or debt securities are listed or in the process of being listed must follow Ind AS.

- **Level II: Unlisted companies with net worth ≥ ₹250 crore , Ind AS is mandatory.

- **Level III: Holding, subsidiary, associate, and joint venture companies must follow Ind AS if the parent/group company is required to comply.

**List of Accounting standards issued by ICAI

| **Accounting Standard | **Description | **Applicable To Level |

|---|---|---|

| AS1 | Disclosure of Accounting Policies | All |

| AS2 | Valuation of Inventories | All |

| AS3 | Cash Flow Statements | 1 |

| AS4 | Contingencies and Events Occurring After the Balance Sheet Date | All |

| AS5 | Net Profit or Loss for the Period, Prior Period Items and Changes in Accounting Policies | All |

| AS6(withdrawn FY 2016-17) | Depreciation Accounting | ----- |

| AS7 | Construction Contracts | All |

| AS8 | Accounting for Research and Development | All |

| AS9 | Revenue Recognition | All |

| AS10 | Accounting for Fixed Assets | All |

| AS11 | The Effects of Changes in Foreign Exchange Rates | All |

| AS12 | Accounting for Government Grants | All |

| AS13 | Accounting for Investments | All |

| AS14 | Accounting for Amalgamations | All |

| AS15 | Accounting for Retirement Benefits in the Financial Statements of Employers | All |

| AS16 | Borrowing Costs | All |

| AS17 | Segment Reporting | 1 |

| AS18 | Related Party Disclosures | 1 |

| AS19 | Leases | All |

| AS20 | Earnings Per Share | All |

| AS21 | Consolidated Financial Statements | See Note |

| AS22 | Accounting for Taxes on Income | All |

| AS23 | Accounting for Investments in Associates in Consolidated Financial Statements | See Note |

| AS24 | Discontinuing Operations | 1,2 |

| AS25 | Interim Financial Reporting | All |

| AS26 | Intangible Assets | All |

| AS27 | Financial Reporting of Interests in Joint Ventures | See Note |

| AS28 | Impairment of Assets | All |

| AS29 | Provisions, Contingent Liabilities and Contingent Assets | All |

**Note: AS 21, AS 23 and AS 27 for the preparation of consolidated financial statements are required to be complied with by a non-corporate entity if the non-corporate entity voluntarily prepares and presents the consolidated financial statements.