Issue of Share for Consideration other than Cash: Accounting for Share Capital (original) (raw)

Last Updated : 10 Jun, 2026

A share is a unit of the share capital of a company that represents ownership in the organization and is evidenced by a share certificate. In simple terms, shares are the divisions or denominations into which a company's total capital is divided. For example, if ABC Ltd. has a total share capital of ₹10,00,000 divided into 10,000 units of ₹100 each, each unit of ₹100 is known as a share. To distinguish one share from another, each share is assigned a unique number. Shares are movable property and can be transferred in accordance with the procedures specified in the company's Articles of Association. According to the Companies Act, 2013, “Share means a share in the share capital of a company and includes stock, except where a distinction between stock and shares is expressly or impliedly made.”

Issue of Shares for Consideration other than Cash:

A company can issue shares not only for cash but also for a consideration other than cash. The shares of a company can be issued for a consideration other than cash to vendors and promoters alsA company may issue shares not only for cash but also in exchange for assets, services, or other valuable consideration. Such an issue occurs when a company acquires assets like land, buildings, machinery, patents, trademarks, or goodwill, or when it compensates promoters, vendors, or service providers by allotting shares instead of making cash payments. The value of the consideration received must be properly assessed and recorded in the company's books. This method helps the company preserve its cash resources while obtaining the assets or services necessary for its operations. The shares issued in such cases are known as shares issued for consideration other than cash and are governed by the provisions of the Companies Act.

1. Issue of Shares to Vendors:

When a company buys some assets and business from vendors, the company can issue them shares in exchange, which is Purchase Consideration.

The amount paid by a purchasing company in consideration for the purchase of assets or business from another enterprise is known as Purchase Consideration****.** Unless it is stated otherwise, the purchase consideration on Net Assets basis is derived as follows:

Purchase Consideration = Agreed value of all assets taken over - Agreed amount of liabilities assumed

**For example, Sahil Ltd. has acquired the assets and liabilities of Kashish Ltd. worth ₹80,00,000 and ₹60,00,000 respectively. Now, the **Purchase Consideration in this case will be ₹80,00,000 - ₹60,00,000; i.e, **₹20,00,000.

**Treatment of Difference between Purchase Consideration and Net Assets acquired:

Case Accounting Treatment If Purchase Consideration > Net Assets The excess of purchase consideration over net assets acquired should be debited to **Goodwill Account. If Net Assets > Purchase Consideration The excess of net assets acquired over purchase consideration should be credited to **Capital Reserve Account.

**Disclosure

The number and class of shares issued for consideration other than cash are disclosed in Notes to Accounts 'Share Capital' in the company's Balance Sheet.

Journal Entries:

**1. On purchase of Business/Assets:

_*The journal entry will include either Goodwill or Capital Reserve

**2. When Assets are purchased:

**3. On part payment to Vendor:

**4. On Issue of Shares:

**A. If Shares are issued to Vendors at Par:

****(b) If Shares are issued to Vendors at Premium:**

**Note:

The number of shares to be given to the vendors in each of the case will be calulcated. The vendor will get the share equal to the asset's purchase price. It means that if the shares are issued at premium, then the vendor will get less shares.

**Formula to determine the Number of Shares to be Issued:

No.~of~Shares~Issued~to~Vendors=\frac{Net~amount~payable~to~Vendor}{Issue~Price~(Net~Face~Value)~of~Share}

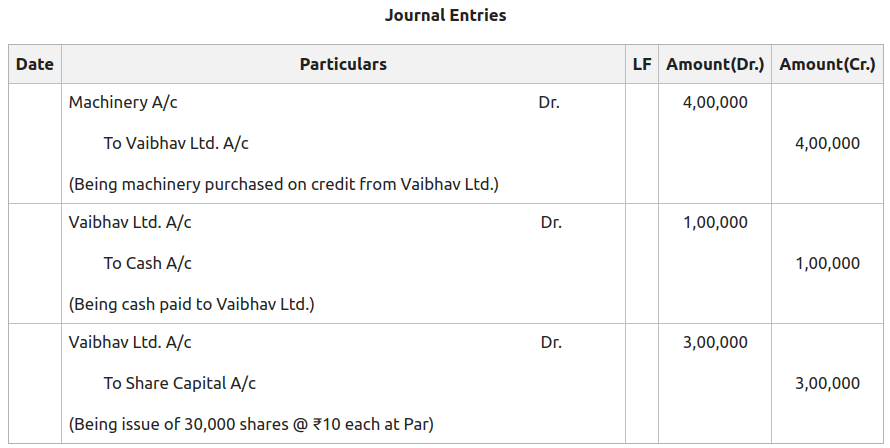

**Illustration 1:

Gaurav Ltd. purchased Machinery costing ₹4,00,000 from Vaibhav Ltd. Payment for the same was made as under:

i) ₹1,00,000 in cash

ii) Balance was payable by issuing shares of ₹10 each at Par.

Pass the necessary Journal Entries.

**Solution:

**Working Note:

No. of Shares of Vendors:

Net amount payable = Total amount payable - Paid in Cash

Net amount payable = 4,00,000 - 1,00,000

Net amount payable = ₹3,00,000

Therefore, No. of shares issued = \frac{3,00,000}{10}=30,000~Shares

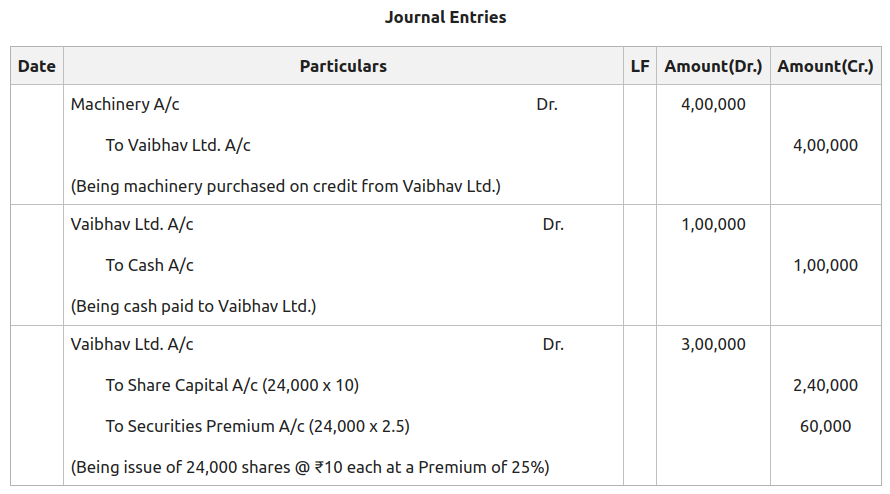

**Illustration 2:

Gaurav Ltd. purchased Machinery costing ₹4,00,000 from Vaibhav Ltd. Payment for the same was made as under:

i) ₹1,00,000 in cash

ii) Balance was payable by issuing shares of ₹10 each at a Premium of 25%.

Pass the necessary Journal Entries.

**Solution:

**Working Note:

No. of Shares of Vendors:

Net amount payable = Total amount payable - Paid in Cash

Net amount payable = 4,00,000 - 1,00,000

Net amount payable = ₹3,00,000

Therefore, No. of shares issued at Premium = \frac{3,00,000}{12.5}=24,000~Shares

2. Issue of Shares to Promoters:

A company can issue shares to its promoters in return for their services towards the creation and establishment of the company. It is the promoter's efforts that play a major role in the creation of the company and its goodwill. Therefore, when the promoters of the company are allotted shares as remuneration, then the Goodwill A/c or Incorporation Cost A/c is debited.

**Journal Entries:

**1. Allotment of shares as remuneration to the Promoters:

**2. On Issue of Shares:

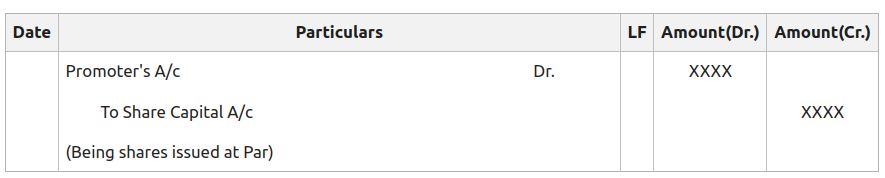

**A. If Shares are issued to Promoters at Par:

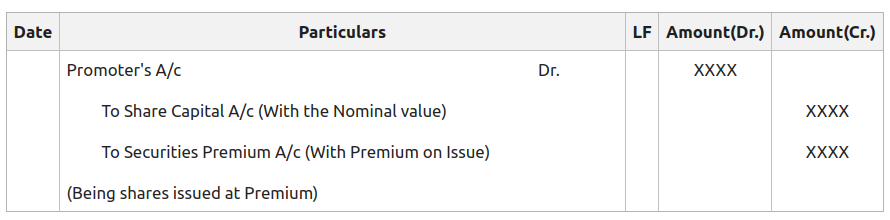

**B. If Shares are issued to Promoters at Premium:

**Illustration:

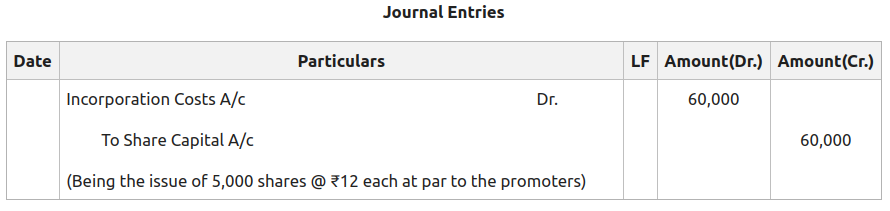

Nisha Ltd. issued 5,000 shares @ ₹12 each credited as fully paid to the promoters of the company for their services. Journalise the transaction.

**Solution:

3. Issue of Shares to Underwriters:

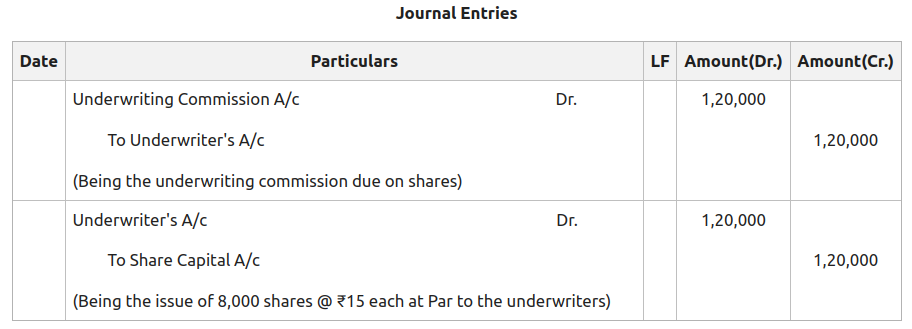

Underwriting is an agreement in which companies enter before the issue and are brought before the public. It is done so that if the shares or debentures are not taken up by the public in full, the underwriters will have to take up and pay for such part of the shares or debentures for which the public has not applied for. Therefore, the underwriters are the persons or institutions who or which guarantee or undertake the issue. For the guarantee given by the underwriters or the services rendered by them, they charge the company with an agreed commission known as Underwriting Commission****.** Instead of paying cash for the commission, the company may allot shares to the underwriters.

**Journal Entries:

**1. On making the commission payable to underwriters:

**2. On payment of commission in the form of shares:

**3. On Issue of Shares:

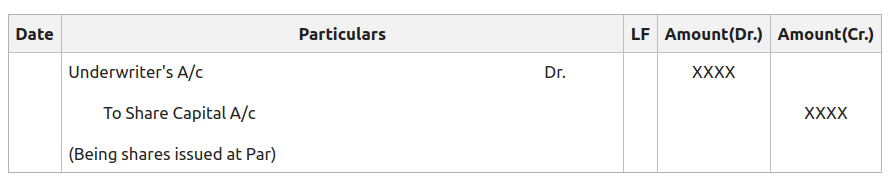

**A. If Shares are issued to Underwriters at Par:

**B. If Shares are issued to Underwriters at Premium:

**Illustration:

Shreya Ltd. issued 8,000 shares @ ₹15 each as fully paid to the Underwriters of the company for their underwriting services. Journalise the transaction.

**Solution: