Calls in Arrear: Accounting Entries with Examples on Issue of Shares (original) (raw)

Last Updated : 10 Jun, 2026

Calls in arrears refer to the amount of money that a shareholder fails to pay to a company on shares for which payment has been requested. When a company issues shares, the amount payable is often collected in instalments known as calls. If a shareholder does not pay any instalment, such as allotment money or call money, by the due date, the unpaid amount is called **calls in arrears. It represents money due from shareholders and remains outstanding until it is paid to the company.

**Journal Entries on Calls in Arrear

1. Without Opening Calls in Arrear Account

Under the first method, the company does not need to open a Calls in Arrear account, and can just credit the actual amount received from shareholders to the call account. The call account, in this case, shows the debit balance equal to the unpaid amount of the call. And when the unpaid amount is received, the Bank A/c is debited, and the relevant Call A/c is credited on that date.

**A. On making the First Call due:

**B. On receipt of the First Call:

**C. On making the Final Call due:

**D. On receipt of the Final Call:

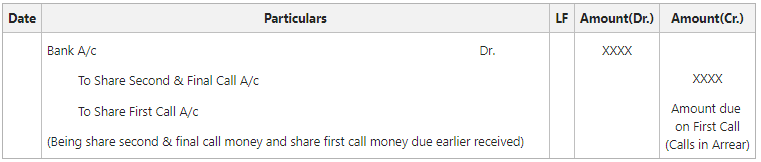

**i. Final call money received without Calls in Arrear:

**ii. Final call money received with Calls in Arrear:

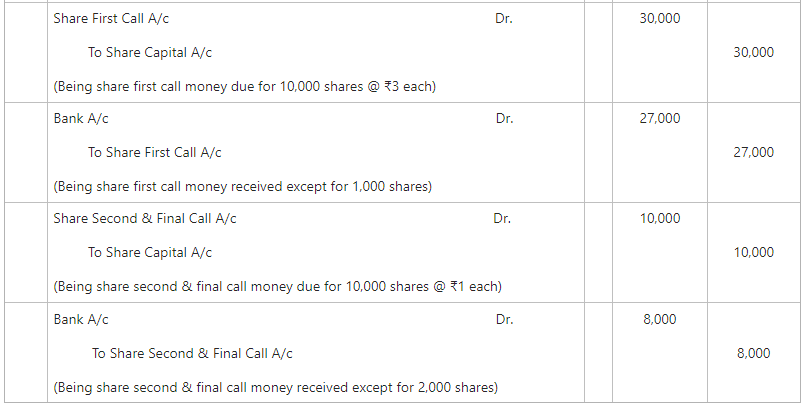

Example of Calls in Arrear (Without Opening Calls in Arrear A/c)

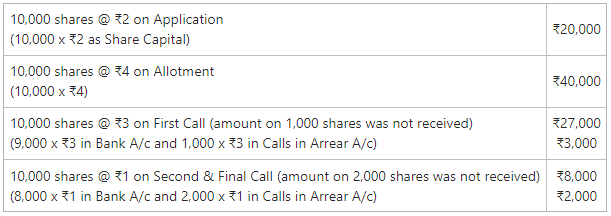

Nisha Ltd. issues 10,000 shares of ₹10 each payable as: ₹2 on application, ₹4 on allotment, ₹3 on the First Call, and ₹1 on the Second & Final Call. The shares were fully subscribed and all money was duly received except First Call money on 1,000 shares and Second & Final Call money on 2,000 shares. Pass necessary Journal Entries without opening Calls in Arrear Account.

Solution:

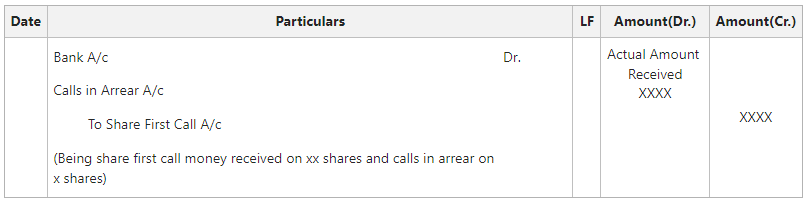

2. By Opening Calls in Arrear Account

Under this method, a separate Calls in Arrears Account is maintained to record the amount of allotment or calls that shareholders fail to pay on the due date. When the unpaid amount arises, the Calls in Arrears Account is debited with the amount due but not received. Subsequently, when the shareholder pays the outstanding amount, the Bank Account is debited and the Calls in Arrears Account is credited. This method helps the company keep a clear record of all unpaid call money until it is received.

**A. On making the First Call due:

**B. On receipt of the First Call:

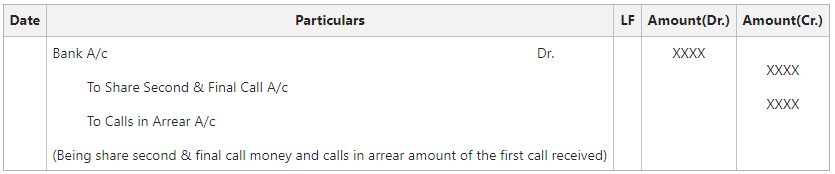

**C. On making the Final Call due:

**D. On receipt of the Final Call:

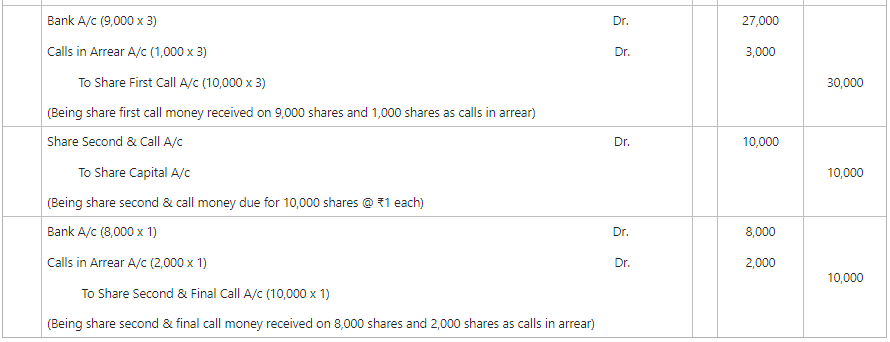

Example of Calls in Arrear (By Opening Calls in Arrear A/c)

Nisha Ltd. issues 10,000 shares of ₹10 each payable as: ₹2 on application, ₹4 on allotment, ₹3 on the First Call, and ₹1 on the Second & Final Call. The shares were fully subscribed and all money was duly received except First Call money on 1,000 shares and Second & Final Call money on 2,000 shares. Pass necessary Journal Entries by opening Calls in Arrear Account.

**Solution:

Interest on Calls in Arrear

A company is authorised to charge Interest on Calls in Arrears from the due date to the date of actual payment at a rate specified in the articles of the company. However, if the articles of the company are silent, then Table F of Schedule I of the Companies Act, 2013 will be applicable for charging interest at a rate not exceeding 10% p.a. Besides, the directors of the company have the right to waive payments of such interests in part or whole.

Journal Entries on Interest on Calls in Arrear

**1. On making due the interest on Calls in Arrear:

**2. On receipt of interest on Calls in Arrear:

**3. On transfer of interest on Calls in Arrear to Profit & Loss A/c at the end of the accounting period:

Example of Interest on Calls in Arrear

Tanya Ltd. issued 70,000 shares @ ₹10 each payable as ₹4 on Application (1st January 2021), ₹3 on Allotment (1st March 2021), and ₹3 on First and Final Call (1st May 2021). Kashish was allotted 1,200 shares and he failed to pay the First & Final Call money on the due date. But he paid the unpaid first & final call money on 1st August 2021 with the interest of 10% p.a. Pass necessary Journal Entries in the books of Tanya Ltd.

**Solution:

**Calculation:

Interest~on~Calls~in~Arrear=3,600\times{\frac{10}{100}}\times{\frac{3}{12}}

= 90