Accounting for Share Capital: Issues of Shares for Cash (original) (raw)

Last Updated : 9 Jun, 2026

A share is a unit of the share capital of a company, representing a portion of ownership in that company, and is evidenced by a share certificate. In simple terms, the total capital of a company is divided into equal parts, and each part is called a share. For example, if a company has a capital of ₹10,00,000 divided into 10,000 units of ₹100 each, then each unit of ₹100 is called a share. To distinguish between different shares, each share is assigned a unique number. Shares are movable property and can be transferred according to the provisions laid down in the Articles of Association of the company. According to the Companies Act, 2013, “shares means shares in the share capital of the company and includes stock except where a distinction between stock and share is expressed or implied.” The capital raised by a company through the issue of shares is known as share capital, which is generally widely distributed among shareholders. In terms of membership, a private company must have a minimum of 2 members and a maximum of 200 members, while a public company must have at least 7 members with no limit on the maximum number. The share capital account is a consolidated account that represents the total amount contributed by all shareholders. A company can issue shares either for cash, through public subscription, or for consideration other than cash, such as assets or services received.

Public Subscription of Shares:

When a company issues shares to the public, it has to take the following steps:

- Issue Prospectus

- Receive Applications

- Make Allotments

- Make Calls

1. Issue Prospectus:

For making an appeal to the public to subscribe for its shares, a Public Limited Company, limited by shares have to issue a prospectus. It is an invitation or a circular given to the general public to invest in the company or subscribe to its shares. The prospectus of a company consists of the following:

- Name and address of the registered office of the company

- Names and addresses of the directors

- Objects of the company

- Risks involved in the issue

- Consent from the Securities and Exchange Board of India (SEBI)

- Authorised and Issued Capital of the company

- Number of shares now offered for subscription

- Terms of the present issue

- Dates of opening and closing of the issue, etc.

2. Receive Application:

After a public company issues a prospectus to the public, it receives applications for shares in a prescribed application form. The company accepts an application only when it is accompanied by the required application money. As per regulations, the application money must not be less than 25% of the issue price per share. This amount is deposited by applicants in a scheduled bank specified by the company at the time of issuing the prospectus. Until the company receives the certificate of commencement of business, it is not permitted to withdraw this application money from the bank. Further, the minimum amount payable at the time of application for each share must not be less than 5% of the nominal (face) value of the share

3. Make Allotments:

After the last date for the application money fixed by the company expires, the bank sends all the applications to the company. However, unless the company has received a **minimum subscription, it cannot go for allotment.

According to **Section 39(1) of the Companies Act, 2013, a Company cannot allot any securities of the company to public unless the amount stated in the prospectus as the minimum amount has been received by the company by cheque or other instrument which has been paid.

Minimum Subscription is the amount, which according to the Directors is the minimum amount raised by the issue of shares so that it can provide:

- The price of any property purchased or to be purchased by the company

- The preliminary expenses payment (including underwriting, brokerage, and commission on the issue of shares)

- The repayment of any money that the company has borrowed for the matters mentioned in the last two points

- Working Capital

- Any other expenditure required to conduct usual business operations.

**According to SEBI, if a company does not receive a minimum subscription of 90% of the net offer made to the public including the devolvement of underwriters within 60 days from the date of closure of the issue, it has to refund the entire amount received for a subscription.

Over-subscription occurs when a company receives applications for more shares than it has issued. For example, if ABC Ltd. offers 10,000 shares but receives applications for 50,000 shares, the issue is oversubscribed five times. In such a situation, the company may reject some applications fully, allot shares partially to some applicants, and accept others in full. Applicants who are allotted shares receive a Letter of Allotment showing the number of shares allotted and the amount payable, while those not allotted shares receive a Letter of Regret along with a refund of their application money.

4. Make Calls:

Once the company has received application money and allotment money, it will call money in subsequent instalments as and when required, which are known as calls****.** A company can demand this amount in one instalment, say on the application itself. However, if the company has not fully called the whole amount on the application, the directors can call for the unpaid amount in one or more instalments. These instalments are named first call, second call, third call, and so on. The time interval between two consecutive calls should be at least one month. The company must make calls strictly in accordance with the provisions of the Articles of Association. If the AOA is not there, then it should apply the Provisions of Table F of Schedule I of the Companies Act, 2013. These provisions are as follows:

- If the total issue size of a company exceeds 250 crores, then the amount to be called up either on application, on the allotment, or calls shall not exceed 25% of the total quantum of the issue. Hence, if the company issues up to 250 crores, then it can call up the entire issue price on the application.

- A company with shares up to 500 crores should fully call up the amount on shares within a period of 12 months from the date of allotment.

- The time interval between two consecutive calls should be at least one month.

- The shareholders must be given notice of at least 14 days to pay the amount of the call.

The call letter of the company must specify the amount of the call, mode of remitting money, address to which call money is required to be sent, and the last date for sending the money.

Preliminary Expenses

The expenses incurred by a company for its establishment are known as Preliminary Expenses. The expenses included under preliminary expenses are as follows:

- Expenses incurred by the company at the time of registration for the preparation and printing of various documents.

- Cost of basic books of accounts and a common seal.

- Stamp duty and registration fees of such documents.

- Duty paid on authorised capital.

- Commission given to underwriters.

- Expenses paid on the preparation and printing of prospectus and issuing of shares.

According to AS-26, a company has to write off preliminary expenses in the year in which they are incurred, and should be written off from the Securities Premium Reserve Account. However, if there is no Securities Premium Reserve Account, then the company can write off preliminary expenses from General Reserve or from Surplus (Balance in Statement of Profit & Loss Account under 'Reserves and Surplus').

**Accounting Entries on Issue of Shares:

1. Entries on Receiving Application Money:

The applicants who want to invest in a company deposit the application money directly in the bank. The bank

then sends the application forms to the company's office.

**A. For entry is made by the company on receiving the application money:

**B. For Application money is transferred to Share Capital A/c (When a share application is accepted, it is an allotment of shares):

2. Entries on Allotment:

The applicants who are allotted shares are sent a letter of allotment. The letter consists of information regarding the number of shares allotted and the amount due to allotment. Once the allotment letter is sent to the applicants, the allotment money becomes due on the allotment and becomes a part of share capital.

**A. For making allotment for money due:

**B. For receipt of allotment money:

3. Entries on First Call:

**A. For entry is passed for call money due:

**B. For receipt of first call money:

4. Entries of Second and Final Call:

**A. For the second call money due as follows:

**B. For receipt of Second Call Money:

**Important Notes

- While passing journal entries, it is essential to use words 'equity'or 'preference' to address the share type. **For example, Equity Share Allotment A/c, Preference Share Application A/c, Equity Share First Call A/c, Preference Share Second Call A/c, Equity Share Capital A/c, etc.

- The last call whether it is first or second, will be called the final call along with its serial number. **For example, First & Final Call, Second & Final Call, etc.

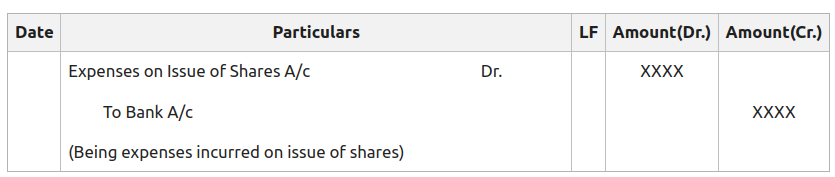

Expenses on Issue of Shares:

A company incurs different types of expenses on the issue of shares. _**For example,_stationery expenses, postage expenses, bank expenses, printing expenses, etc. The expenses incurred on the issue of shares are the capital expenditure of the company. Therefore, these expenses are written off from **Securities Premium Account or **Profit & Loss Account. Until the total amount of capital expenditure is written off by the company, the balance is shown on the asset side of the balance sheet under 'Miscellaneous Expenses' heading.

**Journal Entries:

**1. For payment of expenses on the issue of shares:

**2. For writing off expenses on the issue of shares: