Issue of Shares at Premium: Accounting Entries (original) (raw)

Last Updated : 10 Jun, 2026

A share is a unit into which the share capital of a company is divided, representing a portion of ownership in the company. For example, if ABC Ltd. has a total capital of ₹10,00,000 divided into 10,000 units of ₹100 each, each unit of ₹100 is called a share. Shares are numbered for easy identification and are considered movable property, meaning they can be transferred according to the provisions of the company's Articles of Association. According to the Companies Act, 2013, a share means a share in the share capital of a company and includes stock, except where a distinction between stock and shares is expressly or impliedly made. Thus, a share represents a fraction of a company's capital and ownership

Issue of Shares at Premium:

Issue of Shares at Premium refers to the issue of shares at a price higher than their face value. For example, if a share with a face value of ₹20 is issued at ₹25, the premium amounts to ₹5 per share. Companies are legally permitted to issue shares at a premium without any restriction. The premium received is not treated as a revenue profit but as a capital profit; therefore, it is credited to a separate account known as the Securities Premium Reserve Account. This amount is shown separately on the Equity and Liabilities side of the Balance Sheet under the head “Reserves and Surplus.” According to the provisions of the Companies (Amendment) Act, 1999, the term “Securities Premium” is used instead of “Share Premium

**Utilisation of Securities Premium Account under Section 52 of the Indian Companies Act, 2013:

Under These, when a company issues shares at a premium, the premium amount must be transferred to a Securities Premium Account. Although companies are generally free to issue shares at a premium, the amount standing in this account can be utilized only for specific purposes prescribed by law.

- Writing off the preliminary expenses of the company.

- Writing off the expenses, commission or discount allowed on the issue of shares or debentures of the company.

- For issuing fully paid bonus shares to the shareholders of the company.

- For paying premium on redemption of redeemable preference shares or debentures of the company.

- For buying back its own shares (as per Section 68).

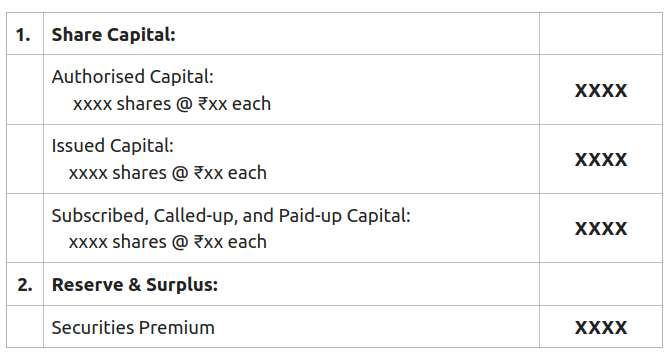

Presentation of Security Premium in Company's Balance Sheet:

**Notes to Accounts:

Accounting Entries for the Amount of Premium:

The company may charge the premium either on application or on allotment or call. Therefore, it is essential to record premium at the time it is payable. The entries for the same will be as follows:

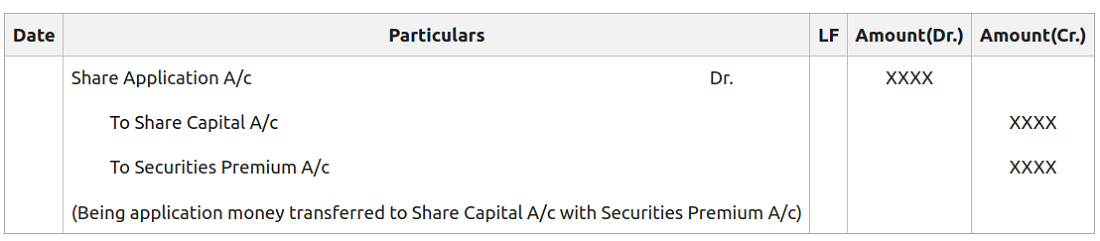

**1. When the Premium amount is received on Application Money:

**A. For receiving Application Money:

**B. For transferring Application Money to Share Capital A/c and Securities Premium A/c:

**2. When the Premium amount is received or receivable along with Allotment Money:

**A. When the allotment money is due including premium:

**B. When the allotment money is received along with premium:

**3. If the Premium is received or receivable with Call Money:

**A. When the call money is due along with premium:

**B. When the call money is received along with premium:

**Illustration 1 (When Premium is received on Application):

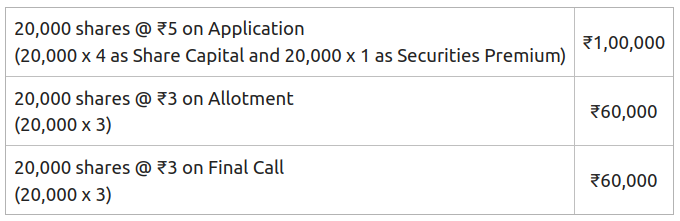

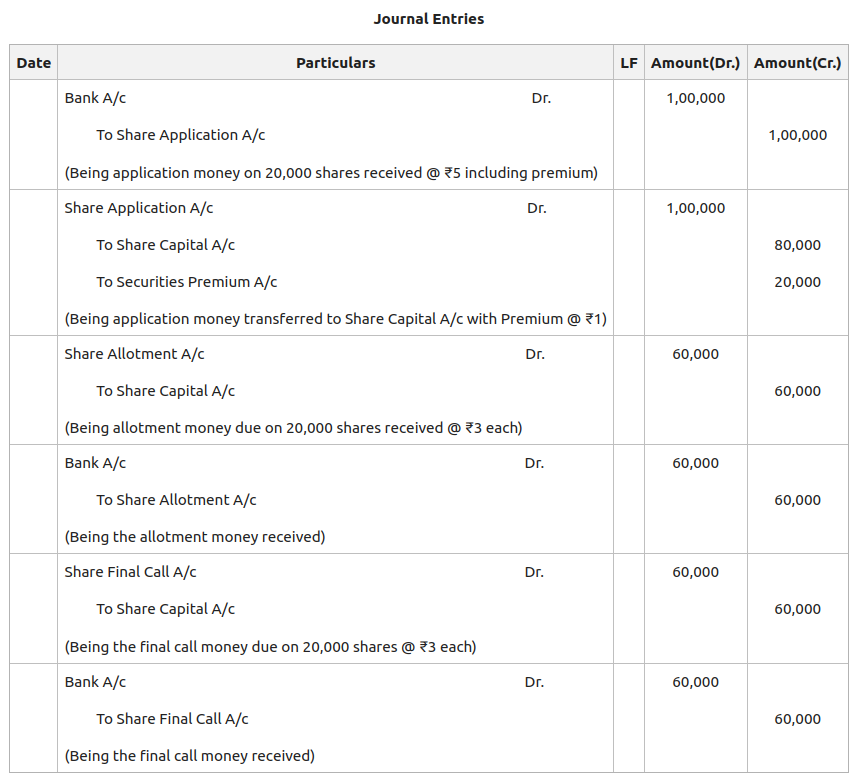

Sukant Ltd. issued 20,000 shares of ₹10 each with 10% premium, payable ₹5 on Application (including premium), ₹3 on Allotment and balance on Final Call. All money was received. Pass the Journal entries in the books of Sukant Ltd.

**Solution:

The amount payable will be as follows:

**Illustration 2 (When Premium is received on Allotment and Call):

Sayeba Ltd. issued 50,000 shares @ ₹10 each at a premium of ₹4 per share payable as follows:

₹3 per share on Application

₹5 per share on Allotment (including ₹2 as premium)

₹3 per share on First Call (including ₹2 as premium)

₹3 per share on Second & Final Call

The issue was fully subscribed and money was duly received. Pass Journal Entries.

**Solution:

The amount payable will be as follows: