Oversubscription of Shares: Accounting Treatment (original) (raw)

Last Updated : 10 Jun, 2026

A share is a unit of the share capital of a company that represents ownership in the company and is evidenced by a share certificate. In simple terms, shares are the denominations into which the total capital of a company is divided. For example, if ABC Ltd. has a total capital of ₹10,00,000 divided into 10,000 units of ₹100 each, each unit of ₹100 is called a share. To distinguish one share from another, each share is assigned a unique number. Shares are movable property and can be transferred in the manner prescribed by the company’s Articles of Association. According to the Companies Act, 2013, a share means a share in the share capital of a company and includes stock except where a distinction between stock and shares is expressly or impliedly made.

Oversubscription of Shares:

Oversubscription occurs when a company receives applications for more shares than the number of shares offered to the public for subscription. This situation generally arises in the case of a sound and well-managed company, where investor demand exceeds the number of shares available. However, a company cannot allot more shares than it has issued for public subscription. In case of oversubscription, the company has three alternatives: it may reject some applications completely, it may make a proportionate allotment of shares among applicants, or it may partially accept applications by allotting a certain proportion of shares and rejecting the excess application money, which is refunded later.

1.First alternative,

Under the first alternative, the company makes full allotment to some applicants and rejects excess applications, and returns the money to those applicants. For example, A company invites applications for 90,000 shares and receives applications for 1,30,000 shares. In this case, allotment of shares will be made as under:

2. Second Alternative:

Under the second alternative, the company makes **pro-rata allotments among the applicants. It means that the company does not reject any application and allots shares to all applicants on a proportionate basis. The excess money paid by the shareholders is then adjusted on share allotment and on subsequent calls unless otherwise mentioned. For example, A company invites applications for 50,000 shares and receives 80,000 applications. Now, the company will allot shares to the shareholders in the proportion of 50,000:80,000; i.e., 5:8. It means that the applicant of 8 shares will be allotted 5 shares. This is known as pro-rata allotment. The excess money of the holders will be adjusted on the allotment and subsequent calls. If after adjusting money on allotment and calls, a surplus amount is left, then that amount will be returned to the shareholders at the time of share allotment.

3. Third Alternative:

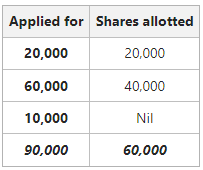

A company may also use a combination of the first two alternatives. It means that a company accepts some applications in full, rejects some applications, and makes pro-rata allotments for the remaining applicants. _For example, A company invites applications for 60,000 shares and receives applications for 90,000 shares. It accepted applications of 20,000 shares in full, rejected applications of 10,000 shares, and allotted applications of 60,000 shares on a pro-rata basis. The allotment will be made as follows:

Accounting Treatment Concerning Oversubscription:

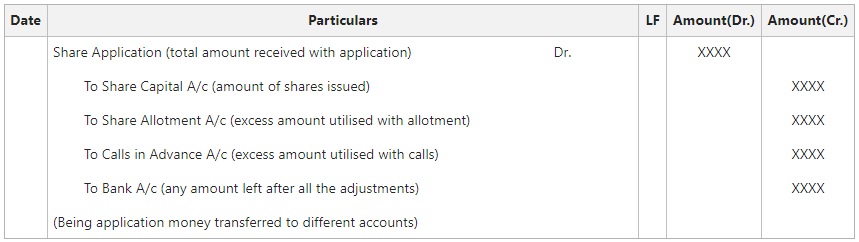

**1. If surplus applications are rejected:

In this case, the application money received from these applicants is returned, and the journal entry for the same will be:

**2. Pro-rata Allotment:

Pro-rata Allotment is a situation in which a company allots shares on a proportionate basis. And adjusts the excess money first on the allotment and then on subsequent calls. If the money still remains in surplus, it is returned to the applicants at the time of allotment. The entry for the same will be as follows:

**3. Full Allotment, Pro-rata Allotment, and No Allotment:

The directors of a company can use a combination of the first two methods. The entry for the same will be as follows:

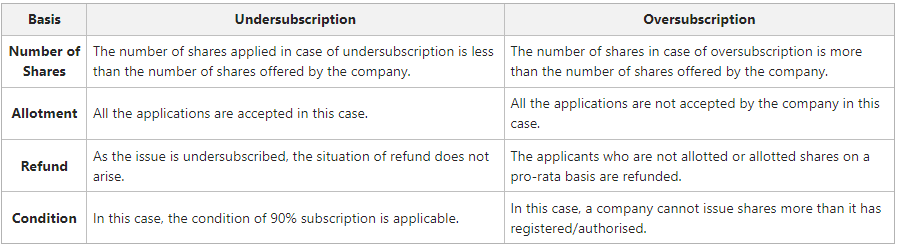

Difference between Undersubscription and Oversubscription:

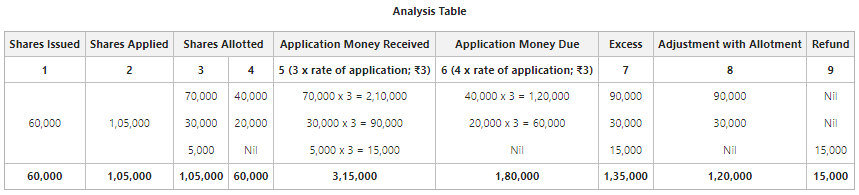

Statement showing the Adjustment of Application Money Received:

When there is an oversubscription of shares, an Adjustment Table can be prepared to show the adjustment of application money received by the company.

**Illustration:

Sukant Ltd. issued 60,000 shares of ₹10 each at a premium of ₹2 per share payable as follows:

₹3 on Application

₹5 on Allotment (including Premium)

₹4 on First & Final Call

Applications were received for 1,05,000 shares. The Directors resolved to allot as follows:

- Applicants of 70,000 shares: 40,000 shares

- Applicants of 30,000 shares: 20,000 shares

- Applicants of 5,000 shares: Nil

Calculate the amount received on Allotment.

**Solution:

**Amount Received on Allotment