IFRS and GAAP (original) (raw)

Last Updated : 20 Feb, 2026

Every company that prepares financial reports needs to follow established standards. These companies must follow either GAAP or IFRS for the applicable rules and guidelines, and financial reports are prepared and published accordingly.

IFRS(International Financial Reporting Standards)

These are a set of accounting standards developed by the International Accounting Standards Board. The main AIM of IFRS is to provide guidance on the preparation and presentation of statements related to finance. IFRS is used in over 140 countries, including the European Union, Australia, Canada, and Japan, and its popularity in other countries is also increasing. The main goal of IFRS is to improve transparency and consistency in financial reporting around the world, making it simpler and easier for investors to compare financial statements from different countries.

Needs for IFRS

With the expansion of international trade and investment, there is a need for a common global language for financial reporting. IFRS provides this common language by establishing a single set of accounting standards that can be used by companies in different countries.it also helps in:

**1. Reduces costs: When businesses use one accounting standard, they can save money by not preparing different financial reports for different countries. This is very helpful for worldwide companies that follow diverse accounting rules in different parts of the world

**2. Consistency and comparability: IFRS ensures that all businesses follow the same rules for financial reports, so it becomes easier to compare them. These helps investors, lenders and other users to understand a company’s financial position clearly.

**3. Better transparency: IFRS requires businesses to be more transparent and provide complete and clear information in their financial reports. This reduces confusion and helps prevent misleading reporting.

**4. More money: When companies are clear about their finances using IFRS, investors in other countries can easily understand and trust their financial reports. This makes it easier for companies to get funding, which is especially helpful in places where investment is hard to find.

GAAP (Generally Accepted Accounting Principles)

These are the rules and guidelines that companies follow to make their financial statements. GAAP makes sure that all companies report their financial info in the same way so that it's easier to compare them.

GAAP is created and maintained by the Financial Accounting Standards Board (FASB), an independent organization based in the U.S. It ensures that financial statements are consistent, accurate, and easy to understand.

Key features of GAAP are:

- **Principles-based: it concentrates on the fundamental logic of accounting instead of strict rules & regulations. This offers more flexibility for individual decisions while following an standards in different situations

- **Rule-based: While GAAP is generally principles-based, there are some areas where it is rule-based. For example, there are strict rules for how companies should recognize revenue and account for inventory.

- **US specific: GAAP is used in the United States. Other countries may have their own rules or use IFRS, but GAAP is specific to the U.S.

- **Historical cost: It follows the historical cost method for valuing assets and liabilities, recording them at their original cost, not current market value. This means some assets may be shown at a lower value than they are worth today.

Ten principles included in GAAP

**1. Principle of Sincerity: Financial reports should honestly reflect the company’s financial situation.

**2. Principle of Prudence: Accountants should be careful and not show income or assets as higher than they really are.

**3. Principle of Permanence of Records: This methods used should remain permanent and consistent so that they can be compared from report to report.

**4. Principle of Continuity: This principle states that all transactions should be done and recorded with the assumption that the business will continue to operate.

**5. Principle of Regularity: There should be regularity in following a specific accounting standard.

**6. Principle of Non-compensation: This principle states that the accountant should record all the transactions whether they are positive or negative.

**7. Principle of Periodicity: All financial data should be well organised and recorded according to the accounting period the data falls into.

**8. Principle of Consistency: Methods & principles of accounting should remain consistent from one period to the next in order to enable accurate comparisons over the time period.

**9. Principle of Materiality: Only material information that could affects financial report & decision making should be recorded.

**10. Principle of Utmost Good Faith: both parties in a agreement must be honest and share all important information. Nobody should hide facts or try to trick the other party.

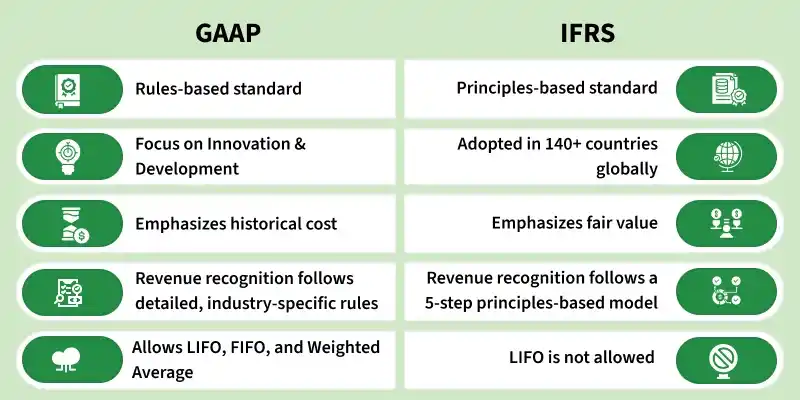

IFRS vs GAAP